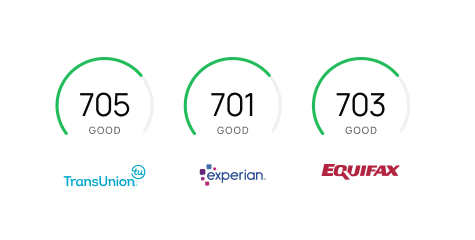

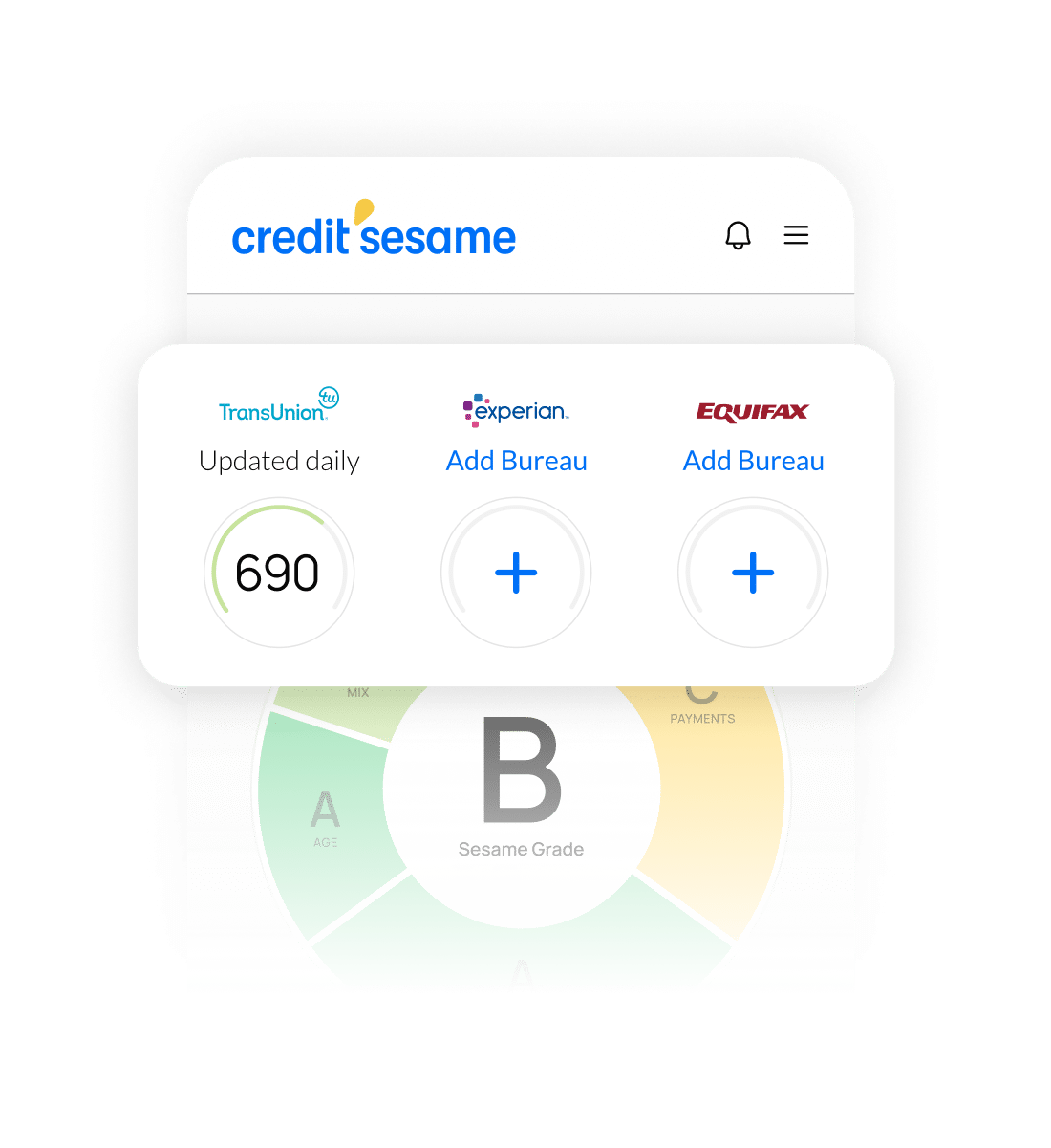

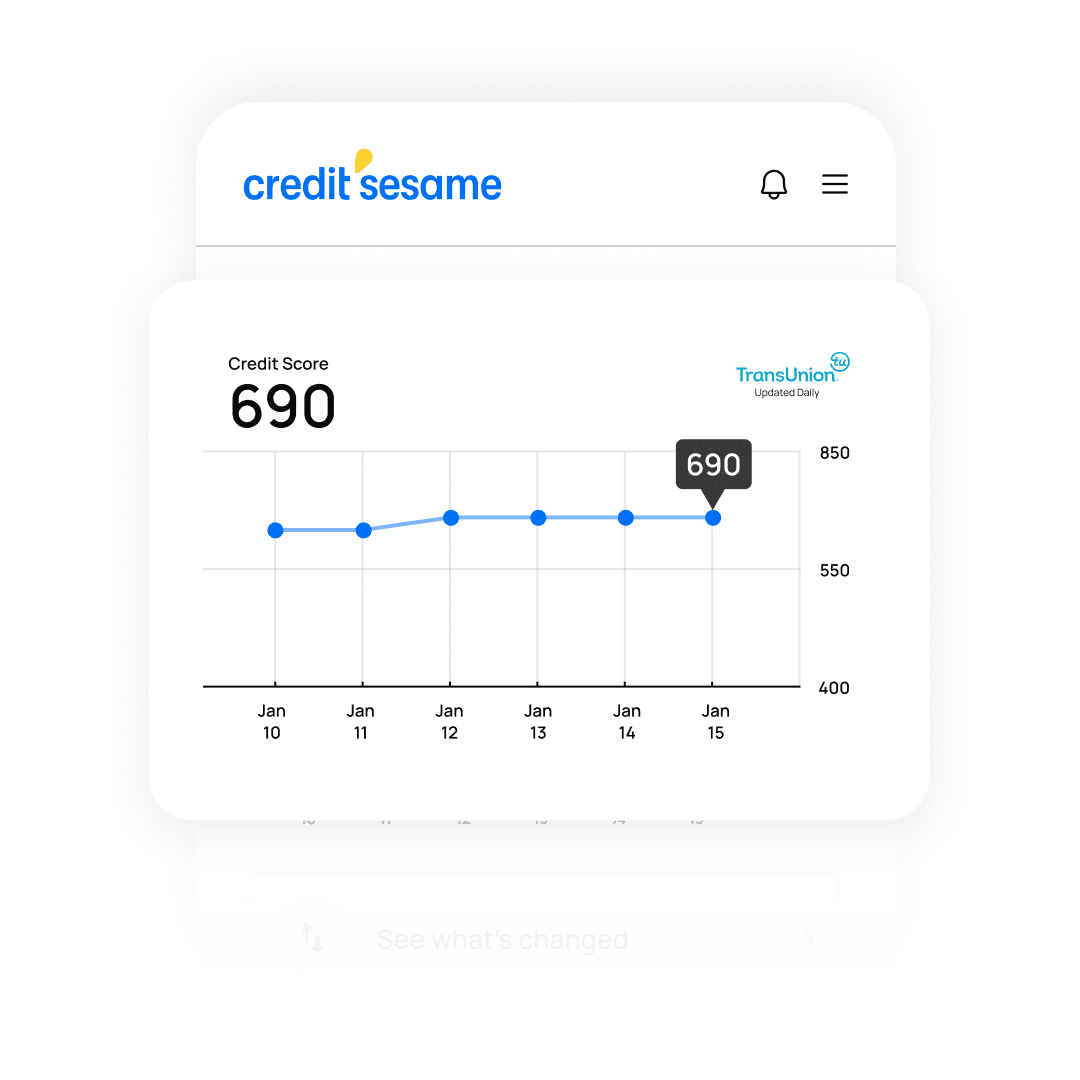

Always know your most up-to-date TransUnion credit score with daily refreshes.

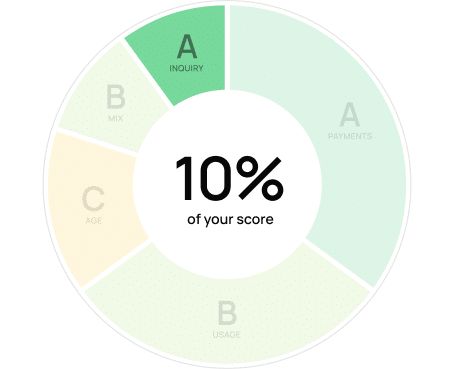

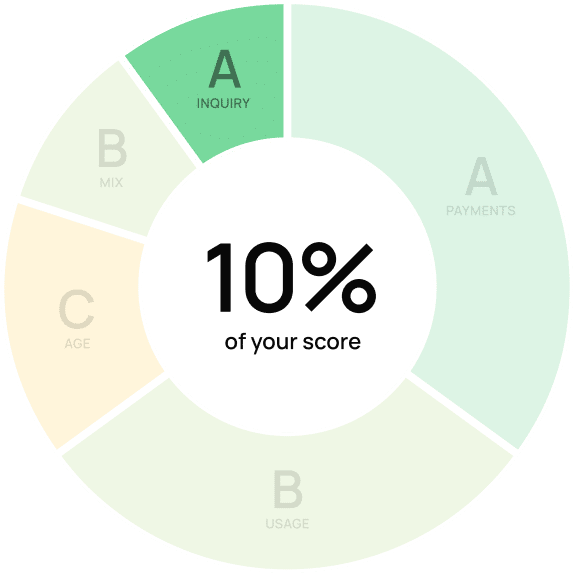

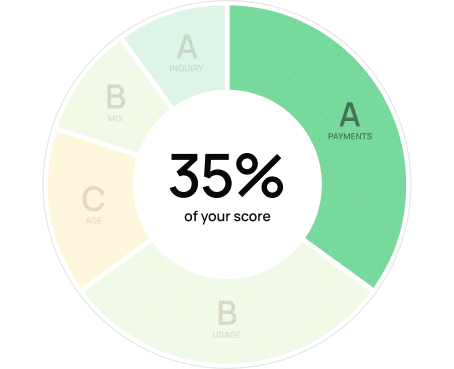

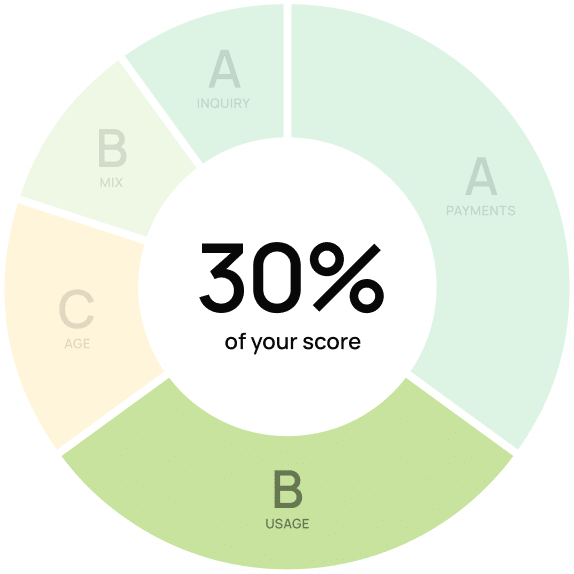

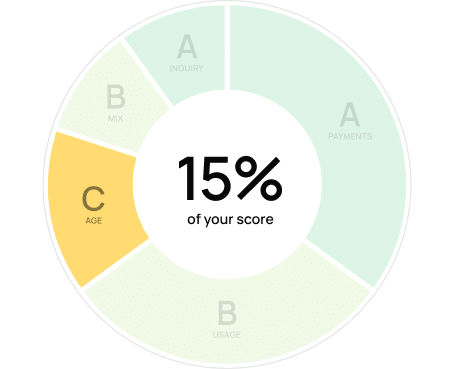

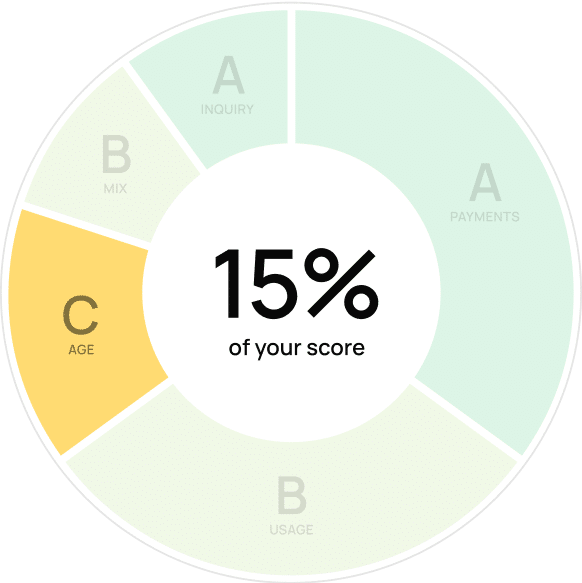

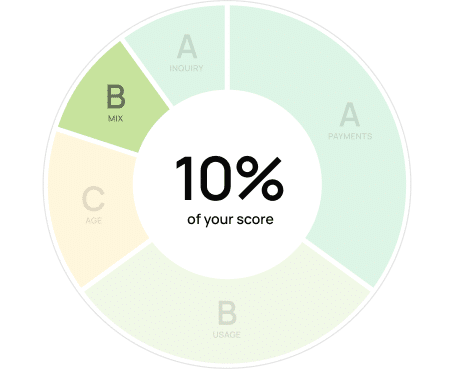

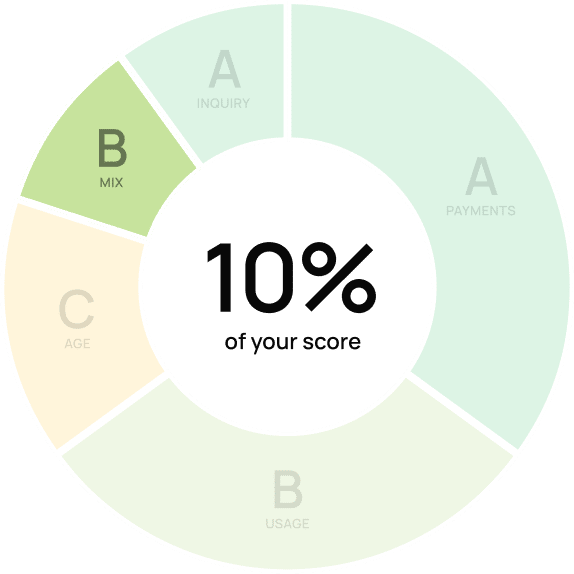

See a clear letter grade based on the five major factors that impact your credit score, including actions to improve.

See a summary of what’s reported on your TransUnion credit report, including open accounts, debts, and more.

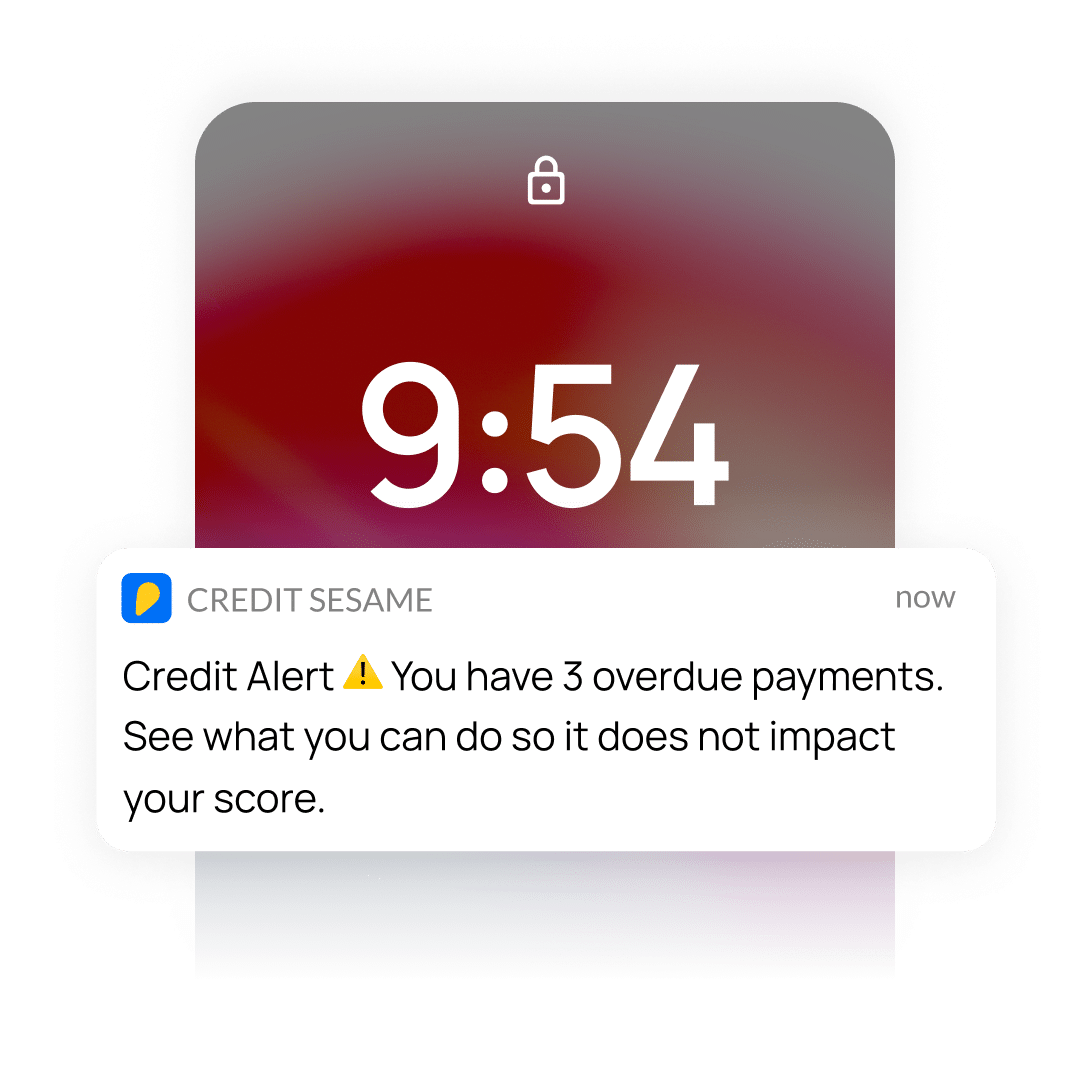

Get notified about changes to your credit file, so you can spot potential errors and protect your score.

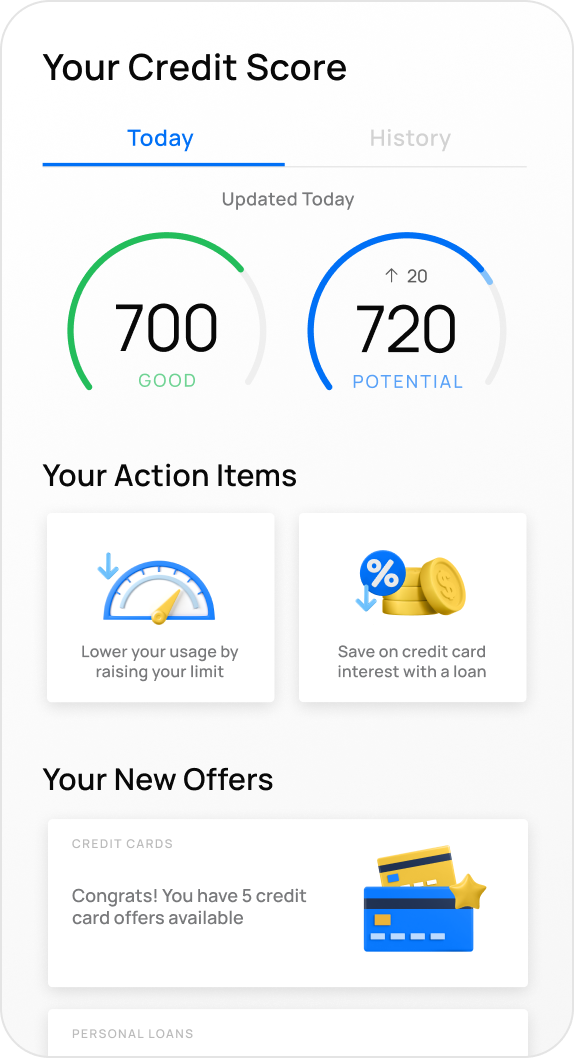

Payment History

Credit usage

Credit age

Account mix

Credit inquiries

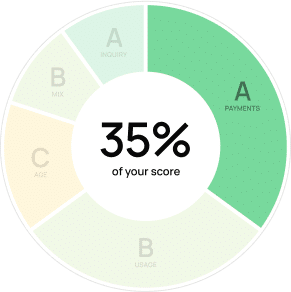

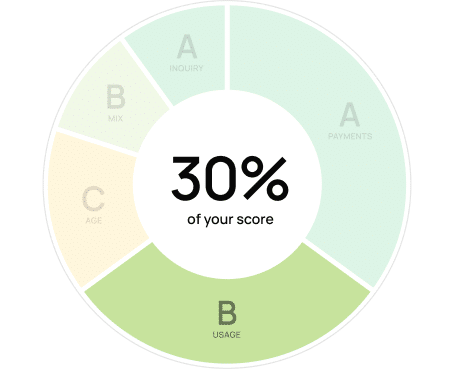

Payment History

Credit usage

Credit age

Account mix

Credit inquiries