Credit Sesame on how interest rate increases do not mean savers hit the jackpot.

Rising interest rates make it more expensive for borrowers because they pay interest. It would seem that rising interest rates are a boon to savers because they earn interest on deposit accounts. Some people win, and some people lose in a kind of equilibrium. However, it is not as simple as that. Borrowers pay much more in interest than savers earn in interest. This has a lot to do with how banks make their money. There are some things savers can do to get a bigger bang from higher interest rates.

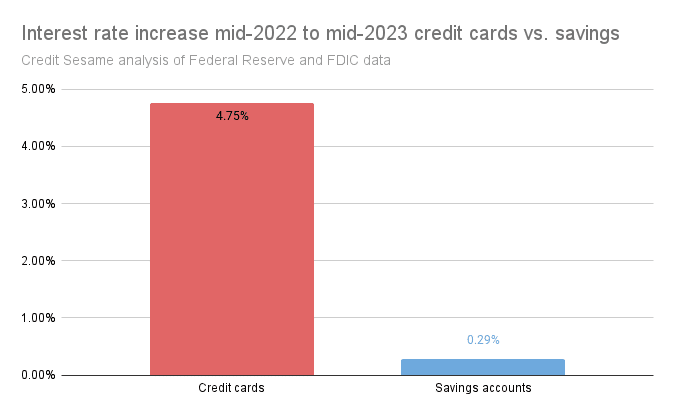

Rates for savers have risen more slowly than rates for borrowers

It is not a secret that borrowers generally pay much higher rates on loans and credit cards than savers earn on deposit accounts. This makes business sense for banks.

Banks take in deposits and use some of that money to make loans and finance credit cards. They charge borrowers more interest than they pay for using the deposits for good reasons.

- Banks facilitate giving depositors a safe and convenient place to keep their money.

- Banks contribute to the federal insurance fund that protects that money.

- Banks bear the expense of processing credit applications and servicing loans and credit cards.

- Banks need to be compensated for the portion of borrowers who don’t repay what they owe.

So far so good. This seems fair. However, banks have taken advantage of the recent rise in interest rates by increasing rates on credit products much faster than they increased rates on savings accounts. An analysis of data from the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC) shows that over the year from mid-2022 to mid-2023, the average credit card interest rate rose by 4.75% while the average savings account rate increased by 0.29%.

Consumers are familiar with this kind of one-sided adjustment to economic changes. Another example is when oil prices change. Rising oil prices seem to be immediately and fully reflected at the pump. When oil prices fall, however, it seems retail gasoline prices take much longer to creep down and often don’t fully reflect how much oil prices have fallen.

Interest rates in general have not kept pace with inflation

Besides not getting their fair share of interest rate increases, savers have been victimized by inflation.

Inflation is the main reason interest rates have risen. Lenders extend credit at a rate higher than inflation to ensure they earn a real return to compensate for risk, opportunity cost and to make a profit. That seems fair to the lender, but the same “fairness” is not extended to savers. Over the past year, the inflation rate has been as high as 9.1%. Meanwhile, savings rates rose to just 0.35%.

Because savings account interest rates barely budged while inflation was soaring, savers are losing more value to inflation. Rather than benefiting from interest rate increases, savers are in worse shape than they were previously.

Shopping around is more important than ever

One thing savers should remember is that they have options. There are thousands of FDIC-insured banks, along with a similar number of federally insured credit unions. The savings account rates offered by these institutions vary greatly. When rates are moving quickly the differences among rates offered by individual banks and credit unions often become wider. Savers may benefit from shopping around. It is worth noting that the biggest, most commonly used banks often have some of the lowest rates. It pays to look beyond the banks with a branch on every corner. With more and more consumers banking online, there is less reason than ever to accept a sub-par rate just because a bank has a lot of branches.

Consider longer-term savings vehicles

If you want to benefit more from higher interest rates, you might consider a Certificate of deposit (CD) instead of a savings account. This means locking up your money for a specified period. However, if you’re able to do that, you can earn more interest.

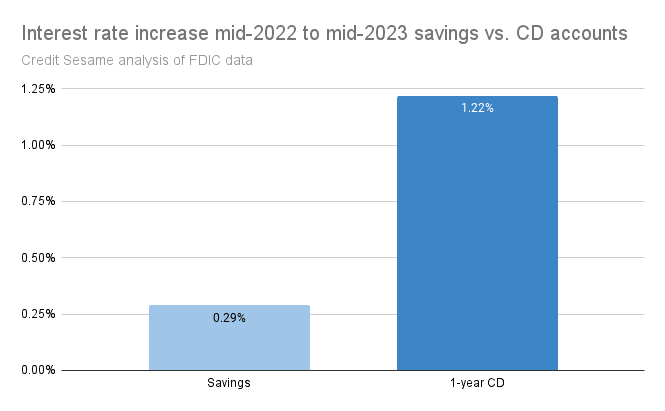

CD interest rate increases more than savings account rates

CD rates are generally higher than savings accounts to compensate for consumers tying up their funds for longer. This normal advantage has grown as interest rates have risen. CD rates have risen faster than savings account rates.

If you don’t want to lock all your money up for a specific period, consider a CD ladder. A CD ladder is a series of CDs that have different maturity dates. This allows you to structure your savings so that part of it becomes available at regular intervals, while you benefit from earning the higher rates offered by CDs.

Are smaller banks riskier than larger banks?

One final word on looking for higher interest rates in this environment. In the wake of bank failures, significant funds were taken out of small- to mid-sized banks. The thinking behind this is that the federal government is more likely to bail out a bank that’s considered “too big to fail.” However, as long as you deposit with FDIC-insured banks and your deposit with any single FDIC-insured bank does not exceed $250,000, your savings are covered no matter what size the bank is. As long as your deposits are insured, the size of the bank does not need to deter you from seeking a better interest rate. If you want to deposit more than $250,000 choose two separate bank accounts and make sure they are not affiliates or subsidiaries of the same parent bank.

If you enjoyed Interest rate increases are not a windfall for savers you may like,

- Open a New Savings Account in 2023

- 9 Money-Saving Hacks for 2023

- Credit card hacks: maximizing card rewards and saving money

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.