Credit Sesame survey reveals characteristics of credit vs debit users.

When you open your wallet to pay for something, what do you reach for?

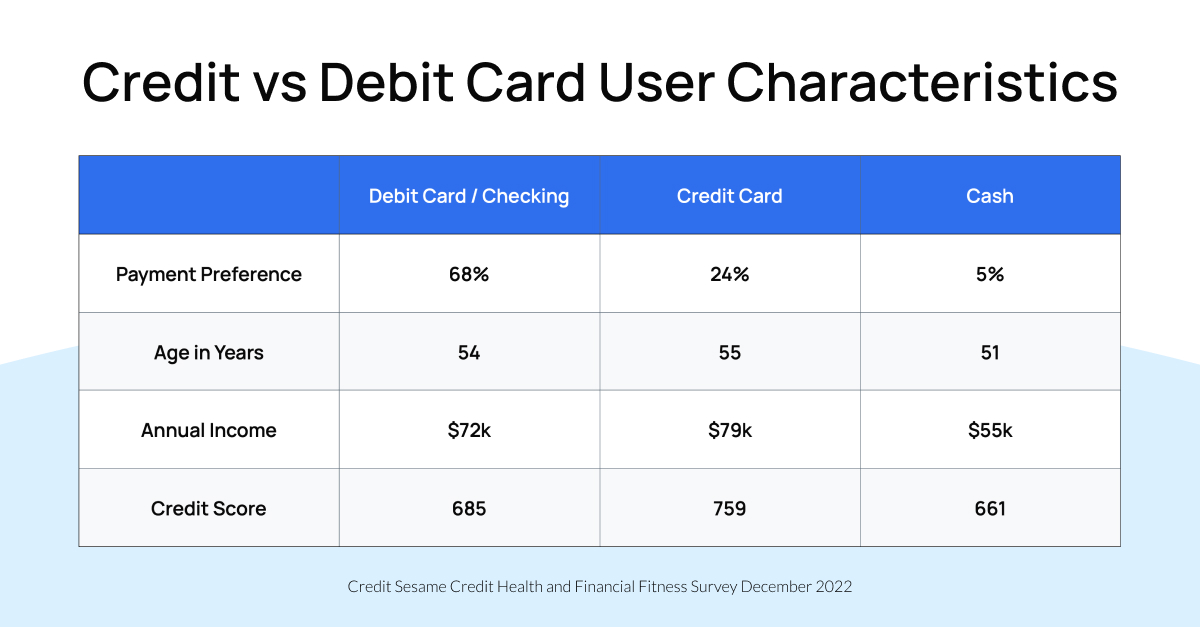

A recent Credit Sesame survey asked over 1,500 American adults what method of payment they are most likely to use for day-to-day expenses. Based on their responses, Credit Sesame looked at the average age, income and credit score for people with each type of payment preference.

The results reveal some distinct characteristics of people who use different types of payments. Your choice, though, should be guided by the pros and cons of each payment method rather than which user characteristics are closest to your own.

Ranking payment preferences

Credit Sesame asked people “how do you usually pay for daily living expenses?”

The top three responses were as follows:

- 68.2% debit card/checking account

- 23.9% credit card

- 5.4% cash

- 2.5% other

Other includes prepaid cards, secured credit cards, Cash App and cashiers check. Interestingly, respondents tended to be in an older demographic (50+ years) and differences in credit score were discernible between debit/checking account users, credit card users and cash users.

Debit card/checking account users

A checking account is a traditional means of managing payments. Accessing money in the account with a debit card or via electronic transfers has mostly replaced writing physical checks.

Though the name “checking account” may be growing somewhat dated, this type of account remains popular. Over two thirds (68.2%) of respondents to the Credit Sesame survey said that using a checking account was their preferred way of paying for day-to-day expenses.

Characteristics of debit card/checking account users

On average, survey respondents who use a debt card/checking account as their preferred method of payment have the following characteristics:

- 53.58 years average age. This makes them very similar to the overall survey average age of 53.83.

- $71,805.64 average annual income. This is a little below the overall survey average of $79,159.14.

- 685 average credit score. That’s pretty good, but it’s a little below the overall survey average of 702

In short, debit card/checking account users are generally of average age, with incomes and credit scores that are a little below average.

Pros and cons of debit card/checking account use

Whether you still write checks, use electronic transfers or a debit card, using a checking account is a sound way of making payments.

Money held in a checking account is usually protected by federal deposit insurance. It may even earn interest, or can be easily linked to an interest-bearing account.

Making payments out of a checking account means using money you already have. That way you don’t run the risk of incurring interest charges by borrowing money.

On the downside, debit cards don’t offer quite as strong fraud protections as credit cards. Writing checks may be even more risky, because you’re sharing your bank account number with anyone you pay by check.

Another disadvantage of debit cards is that using them does not help you build a credit history.

Credit card users

Credit cards came in second to debit cards in this survey. They were the primary payment choice of 23.92% of respondents.

Credit cards are very popular with consumers and Americans now have over a trillion dollars in credit card debt outstanding, an all-time high.

That heavy debt load is a reminder that there is a right way and a wrong way of using credit cards. As a short-term cash substitute, they are useful. As a form of long-term borrowing though, they are expensive and inefficient.

Characteristics of credit card users

Credit card users in this survey are:

- 55.11 years average age. That makes them older as a group than the overall survey average and older on average than the users of any other form of payment.

- $106,445.80 average annual income. This is much higher than the overall survey average of $79,159.14.

- 759 average credit score. The responders in this group using credit cards as their primary form of payment have excellent credit. Their average score of 759 is significantly higher than the overall survey average of 702.

In this survey, people who use credit cards primarily are older, more affluent and have better credit than those who choose debit cards or cash.

Pros and cons of credit card use

A great thing about credit cards is their efficiency. Instead of carrying cash around or depleting your checking account, you put purchases on your credit card and then pay them off once a month.

If you pay your balance off in full every month, you can avoid interest charges. If your card has no annual fee, that means you can use a credit card for free.

On top of that, some credit cards offer rewards which can reduce the net cost of things you buy. Credit cards also have strong protections against fraud.

Using credit cards can help you build your credit history. This works to your advantage if you use the card regularly but make all your payments on time and keep your balance to a minimum.

The downside of credit cards is that many people do not pay their balances off from month to month. This means incurring interest charges. Credit card annual interest rates are very expensive. The average in early 2023 is above 20%. For people with poor credit scores, it can be much higher.

Cash users

Only 5.40% of survey respondents said they use cash as their primary method of payment.

Characteristics of cash users

As a group, people who still use cash for most things have the following characteristics:

- 51.45 years average age. These respondents are generally younger than the overall survey average and younger than debit and credit users.

- $54,923.43 average annual income. This is well below the overall survey average.

- 661 average credit score. This is significantly below the survey average of 702.

These characteristics may highlight that it can be tough for younger and lower earners to establish credit. There may also be a chicken-and-egg aspect situation. People who do not use credit regularly do not build their credit scores.

Pros and cons of using cash

The nice thing about cash is that it doesn’t cost you anything to use – not directly, anyway.

Also, anyone can use it. You don’t need to open an account anywhere to use cash.

On the downside, cash can be risky because it’s subject to theft or loss. It can also be inconvenient. It can be hard to get your hands on cash unless you have a bank account and an ATM card.

Keeping cash outside a bank means you do not earn any interest. Also, using cash does not build a credit history.

Do you have to choose credit vs debit?

The good news is that these payment methods are not all-or-nothing choices. You can use debit, credit and cash from time to time. Thinking about the pros and cons of each can help you choose the right method for different situations.

Survey methodology

The Credit Sesame Credit Health and Financial Fitness Survey December 2022 was designed and executed by Credit Sesame using the WebEngage survey tool. The survey sample comprised over 1,500 Credit Sesame members with a credit score distribution resembling the U.S. general population. In aggregate the sample data is accurate with a 2.5% margin of error using a 95% confidence level.

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.