Credit Sesame discusses using health savings to build retirement wealth.

The recent surge of inflation increases the cost of a comfortable retirement. To meet that cost, it’s more important than ever to make the most of your retirement-saving opportunities.

Besides traditional retirement savings vehicles such as 401(k) plans and IRAs, a Health Savings Account can be a valuable tool for building retirement wealth. Employees often use these accounts to help meet year-to-year medical expenses. However, health savings accounts have special advantages that can help you accumulate long-term retirement savings.

What is a Health Savings Account?

A Health Savings Account (HSA) is a tax-advantaged savings account for paying healthcare expenses.

Contributions to an HSA are tax-deductible, just like contributions to a traditional 401(k) or IRA. The difference is, withdrawals from HSAs are not taxable as long they’re used for qualified medical expenses.

To participate in an HSA, you must enroll in a high-deductible health plan (HDHP). An HDHP is a form of health insurance with a higher deductible than most health plans.

That high deductible means that you may face more out-of-pocket costs. In return, HDHPs typically have lower premiums than other health insurance plans. This can be an especially cost-effective approach to health insurance for people who are generally healthy and don’t expect much in the way of annual medical expenses.

Where an HSA enters into this is that it can help people build up a reserve of savings to meet the higher-out-of-pocket expenses that come with an HDHP.

Both employees and their employers can make contributions to an HSA. There are annual limits to the combined amount employers and employees can contribute to an HSA. For 2022, that limit is $3,650 for someone with individual coverage. For someone with family coverage, the total annual contribution limit is $7,300.

These contributions can be used to meet out-of-pocket medical expenses. Any amount you don’t use in a given year can be kept in the HSA and used for future medical expenses.

Build retirement wealth with your HSA

That ability to accumulate money in an HSA from year to year is a key to why they can be used for more than just meeting near-term medical expenses. They can also build long-term retirement wealth.

In fact, when it comes to retirement savings, HSAs have a superpower that 401(k) plans and IRAs don’t have. HSA savings can be completely tax free.

401(k) and IRA money is subject to taxation either before it goes into the plan (in the case of a Roth plan) or when it’s taken out (in the case of a traditional plan). On the other hand, contributions to an HSA are tax-deductible. Money taken out of an HSA isn’t taxed as long as it’s used to pay qualified medical expenses.

That tax advantage makes it worthwhile to accumulate money in an HSA. That means using this type of account for more than near-term, out-of-pocket expenses. You can also use it to build retirement wealth, as long as you ultimately use the money for medical expenses.

With this in mind, you can invest some of your HSA money for long-term growth while keeping a portion of it liquid for nearer-term expenses. In that sense, it can function like a retirement account. The difference is, an HSA has the added advantage of not being subject to taxation at any time.

Healthcare is a large portion of retirement expenses

The obvious limitation to using an HSA for retirement savings is that the money has to be used for medical expenses. So, an HSA does not work as your only source of retirement savings.

However, since healthcare is a significant portion of retirement expenses, an HSA can play a big role in helping you save for those expenses.

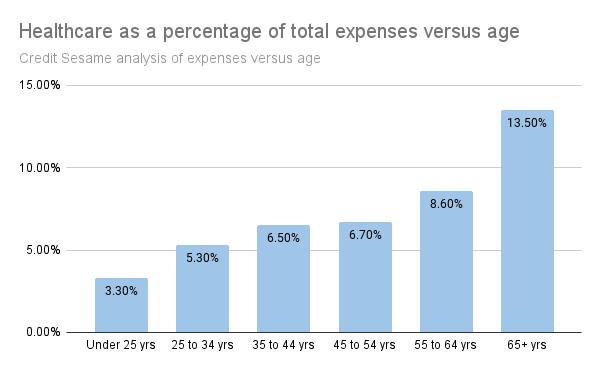

The chart below uses Bureau of Labor Statistics data to show how healthcare becomes a bigger portion of expenses as people age:

On average, based on the percentage of total expenses, people 65 years and older spend twice as much as people in their late 30s and early 40s.

An HSA is the most tax-efficient way of meeting healthcare expenses. You can use your HSA to prepare for those expenses by doing the following:

- Contributing more to an HSA than you need for year-to-year expenses, so you start to accumulate a larger balance over time.

- Investing a portion of your HSA for long-term growth.

HSA contributions vs. 401(k) contributions

If you are eligible for both an HSA and a 401(k) through your employer, how do you decide which to use?

In most cases, you should contribute to both. Each has an important role to play.

- As noted, HSAs have a tax advantage over 401(k) plans when used for qualified medical expenses. They should represent a portion of your retirement savings earmarked for healthcare expenses.

- There are plenty of other retirement expenses besides healthcare. Your 401(k) plan can be used to save for those other expenses.

A key to deciding between contributions to an HSA or a 401(k) is the type of employer match available on each. Employers can contribute to both types of plans on their employees’ behalf. Often, they match a portion of the contribution that their employees make.

If your 401(k) plan has a more generous matching formula than your HSA, you may want to contribute enough to the 401(k) to make the most of the employer’s match. Beyond that amount, you should look to put money into the HSA.

HSA vs. IRA contributions to build retirement wealth

The choice is a little simpler when it comes to deciding between HSA and IRA contributions.

There is typically no employer match available for an IRA. So, the superior tax advantages of HSAs should make those contributions to an HSA more attractive. However, since you have retirement expenses besides healthcare, you should also work on building up a balance in your IRA.

Contributions to HSAs, 401(k) plans and IRAs are each subject to annual limits. That’s a final reason to use an HSA to supplement your retirement savings. Doing so allows you to build tax-advantaged savings beyond the contribution limits on 401(k) plans and IRAs.

You may also be interested in:

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.