Credit Sesame discusses personal finances through the ages.

People measure financial success in different ways. For young people, it may be having a lot of disposable income rather than just making ends meet. When you’re starting a family, it might be owning the biggest house in the neighborhood rather than renting an apartment. For older people, it might be having a comfortable nest egg safely stashed away for retirement rather than living off a meager pension.

Partly this is a matter of personal taste and values, but needs and circumstances change as you get older. This means you may need to rethink what financial success looks like as you age. How does your financial situation evolve over your adult life? What goals might you pursue at each stage to enjoy financial success at all ages?

How personal finances change with age

Credit Sesame assembled some information on income and expenses from the Bureau of Labor Statistics and net worth and debt from the Federal Reserve’s Survey of Consumer Finances. Plotting that information across different age groups creates a picture of how personal finances typically evolve as a person ages.

Income and expenses

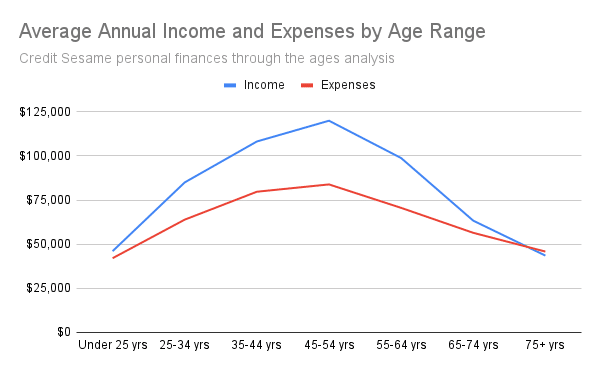

Starting with the most basic measures of personal finances, the graph below shows how average annual income and expenses change across different age groups:

The blue line in the chart shows the average annual income for each age group. Not surprisingly, this starts low. Most people begin their careers at the bottom of the income ladder. Fortunately, though, earning power usually increases over time.

For most Americans, income peaks in their late 40s and early 50s. Then it starts to decline as their careers wind down and they retire.

Now, look at average annual expenses, which are represented by the red line. These start relatively low for younger people. That’s appropriate because their incomes are low at that stage.

Then, as people get older and their incomes grow, they typically improve their lifestyles, and their expenses also increase. Like income, expenses tend to peak when people are in their late 40s and early 50s.

However, note the space between the two lines. Even as both income and expenses grow, the gap between the two lines widens. That means income typically grows faster than expenses at that stage. As a result, this is when people’s ability to save money peaks.

Finally, note that the two lines cross at the far right side of the chart. At that point, retirement income may not be enough to meet expenses, so it’s essential to have savings to fall back on.

Debt

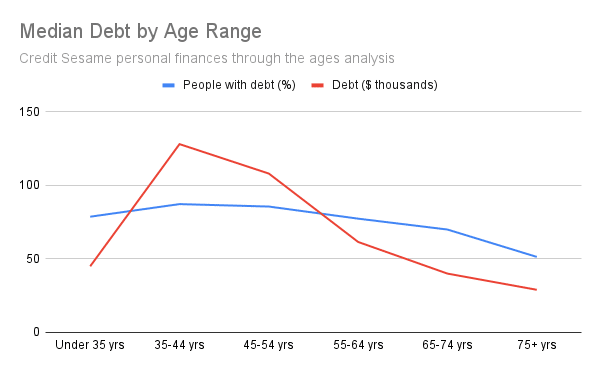

People borrow money throughout their adult lives for different reasons. Perhaps starting with student loans, moving on to car loans and credit card debt after graduation, and finally, a mortgage. The chart below illustrates the percentage of people with debt at different ages.

The blue line shows the percentage of each age group that has debt. Note that most people typically have some form of debt throughout their adult lives. Many start with student loan debt, then they start to add other forms of debt on top of that. However, by the time people move into their late 40s and early 50s, more and more start to become debt-free, so the percentage of people with debt declines from then on.

In dollar terms, this peak and eventual decline are even more dramatic. The average amount of debt in dollars is shown by the red line. Debt peaks when people are in their late 30s and early 40s because this is typically when they take on mortgage debt. Fortunately, most people start paying down their debt steadily from that point forward.

Assets and net worth

People’s progress in accumulating wealth over time can be measured by their assets and net worth. The difference between assets and net worth is that assets are things you own, while net worth is the value of the things you own minus any debt you have.

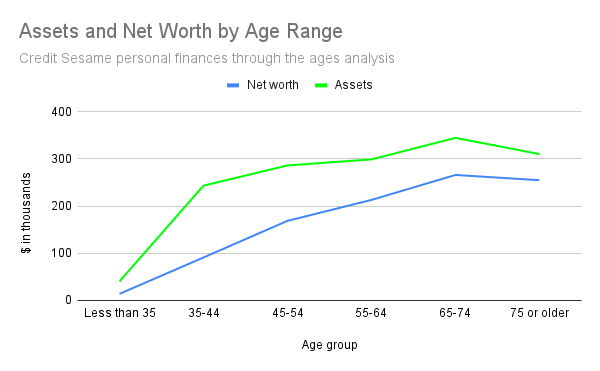

Here’s how assets and net worth change over time:

The green line shows the average value of people’s assets. This increases sharply as people move into their 30s and 40s. The blue line shows net worth. This also grows, but less sharply than the value of assets. That’s because people often use debt to acquire some of those assets. That debt subtracts from net worth.

Over time though, the gap between the two lines narrows. This is because people are paying down debt, so they own more of their assets free and clear. Significantly, both assets and net worth continue to grow until very late in life. Only then, when most people have to live off their savings, both start to decline.

Personal finances through the ages

The pattern of how personal finances change over time should guide the type of goals you set for each stage of life.

Early stage goals

As you leave school and move into the workforce, your primary concern may be making ends meet. Still, there are things you can do to start setting yourself up for financial success:

- Establish credit. Getting credit accounts and establishing a good payment history allows you to access credit when you need it for bigger things, like buying a car or a home.

- Make a budget. Don’t just wing it. Based on your income, plan how you will meet your expenses, including debt obligations.

- Begin paying back any education loans. Starting by making your student loan payments on time is a great way to build a credit history.

- Set aside some emergency savings. Besides paying the bills, your budget should also leave room for savings. Start by setting aside six months’ worth of expenses in case of a financial setback. Once you get into the savings habit, you can move on to longer-term savings.

Mid-life earning goals

As you move into your late 30s, you should be approaching your peak earning years.

- Maintain excellent credit. Even though your income should be enough to meet routine expenses, credit remains important for larger purchases. Keeping your credit score up qualifies you for lower interest rates – which means more of your money can go toward building wealth.

- Make long-term career and housing plans. Now’s the time to make critical decisions about your career and how you want to live. Decide on the best career track for your interests and skills. Consider whether you want to be a renter or a homeowner, and plan accordingly.

- Grow income faster than expenses. It’s okay to upgrade your lifestyle as your income grows. Just make sure your income is growing more quickly than your expenses. This period is when the gap between income and expenses should be widest, with income outpacing expenses.

- Start saving for retirement. Retirement may be 20 or 30 years away, but now’s the time to plan for how much you need to save. Early savings have the most chance to grow by the time you retire, and a comfortable retirement depends on making the most of saving during your peak earning years.

Late-stage goals

As your career winds down, your finances should adjust:

- Pay off debts. Taking on debt is one thing when you have many years to repay it. As you get later in your career, you should be paying down those debts, so you won’t be as burdened by payments once your income starts to decline. Ideally, it would be best if you retired your debts before you retired.

- Identify retirement expenses. As you move closer to retirement, you should be able to get a better handle on living expenses during retirement.

- Plan your retirement distributions. If you plan to draw on savings from a 401(k) or other retirement account, the amount you use each year requires careful planning. You need to meet minimum distribution requirements, plus use your money at a pace that sustains you throughout retirement.

- Work out the timing of key decisions. The timing of when you retire and when you start taking Social Security are crucial to how much money you have to live on in retirement. Both depend on your individual circumstances, but even these late-stage decisions require thinking long-term.

Financial success means different things to different people. However, even your own measures of success may change as you age. Clear goals for income, expenses, debt, and net worth over time can help you keep your personal finances in order at any age.

You may also be interested in:

- What Is Your Personal Finance Dashboard Telling You?

- Improve Your Finances With a Passive Income Stream

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.