Credit Sesame discusses the pros and cons of buy now pay later.

It sounds like such a good deal. If you get to buy now and pay later, isn’t that a win for you?

The deal sounds especially appealing when Buy Now Pay Later plans advertise that they have no interest charges.

Still, as with most financial deals that are touted as all upside, Buy Now Pay Later deserves a closer look before you sign up.

How Buy Now Pay Later Works

Buy Now Pay Later (BNPL) is a type of payment program that lets you walk out of a store with a purchase by just putting down a partial payment – often 25%. You then pay the remaining amount according to a set schedule.

To use BNPL, you sign up with a firm offering this form of payment service. Some of the leading firms in BNPL are Affirm, Afterpay, Klarna, PayPal and Zip.

You can apply to a BNPL program through an app on your mobile phone. If you are approved, you can then use the app at participating merchants much like a credit card. However, there are two key differences between Buy Now Pay Later and using a credit card:

- With BNPL you put some money down initially, which you don’t do with a credit card

- Unlike a credit card, BNPL does not charge you interest on the unpaid portion of your balance as long as you pay it off within the payment schedule

That payment schedule is the key. Once you make your purchase, the BNPL company pays off the merchant. After that, you owe the remaining balance to the BNPL company. If you don’t make your payments on schedule, you could face stiff penalty fees. There may also be a monthly fee just for participating in a BNPL program.

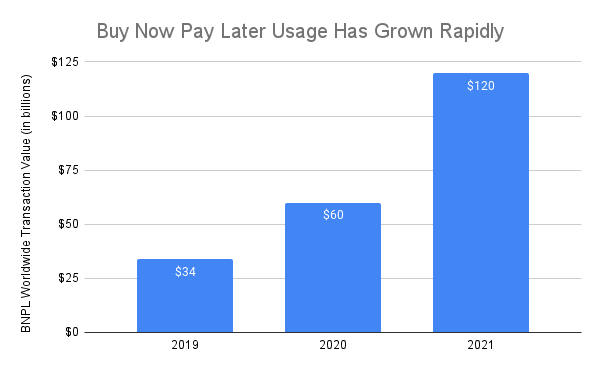

The Sudden Growth of Buy Now Pay Later

BNPL has become an international phenomenon. Besides the United States, BNPL has gained popularity in Australia, Sweden, Germany and the UK.

With this broad popularity, usage of BNPL has grown rapidly. Below is a chart showing worldwide BNPL transaction volume over the past three years, according to GlobalData:

One reason for the rapid growth of BNPL programs is that it’s easy to get approval. The application process is quick and requires less information than a typical credit card application. This has made BNPL an attractive alternative for people with limited or poor credit histories.

Why Regulators Are Concerned

The sudden popularity of BNPL has gotten the attention of financial regulators in a variety of countries. Here in the United States, the Consumer Financial Protection Bureau (CFPB) has sent a letter to five major BNPL providers requesting more information about how they operate.

Why is the CFPB concerned? Here are a few reasons:

- Potential to increase debt. Access to BNPL programs may be too easy. People who lack a history of using credit responsibly might find themselves using BNPL for lots of routine purchases. Taking on months’ worth of debt to pay week-to-week expenses creates a debt snowball.

- Lack of clarity on cost. While BNPL programs often tout that they don’t charge interest, in effect the late fees on purchases may function as interest — and at a very high rate. Charging customers via these fees rather than a percentage interest rate can make it hard to compare the cost of BNPL programs with traditional credit alternatives.

- Inadequate disclosure. Some BNPL programs many be using the newness of the approach to assume they are not covered by the same consumer protection laws as credit card customers. This may mean they aren’t providing consumers with enough information before they sign up.

- Lack of consumer protections on disputed transactions. Credit cards have rules that govern how disputed transactions are resolved. This can be especially important for resolving fraudulent transactions in your account. BNPL programs do not provide the same protections.

At this point, regulators aren’t accusing BNPL companies of doing anything wrong. They just want supervision of these programs to catch up with their rapid growth.

How Does Buy Now Pay Later Affect Your Credit History?

Since BNPL programs are available to people with limited or poor credit, you might think they’d be a way to establish or rebuild credit. However, this is not necessarily the case.

According to the CFPB, most BNPL payments are not reported to credit bureaus. So, even if you use BNPL regularly and responsibly, it may have no effect on your credit history.

On the other hand, late payments may be reported, especially if they are referred to a collection agency. In that case participation in a BNPL program could hurt your credit record.

Thus, while BNPL may be available to people without a strong credit history, it may not be a pathway to establishing credit. In fact, there’s a chance it could do more harm than good.

What You Should Know Before You Buy Now Pay Later

As with many financial tools, BNPL isn’t all good or all bad. Whether it works for you depends on the terms of the specific program and how you use it.

In order to use BNPL effectively, here are some things you should think of first:

- Plan before you spend. BNPL really amounts to making a down payment and then borrowing the remaining purchase price. That makes it important to budget for how you’ll pay off the rest of the purchase. Budgeting before you borrow will help you avoid ramping up debt faster than you can pay it off. It will also show whether you’ll be able to pay off the purchase before any late fees kick in.

- Check the monthly fee. Think about what participating in a BNPL program would cost you over the course of a year. Is that much money worth it compared to how much you’d use the program? Are there cheaper alternatives like a no-fee credit card?

- Know your payment schedule. Don’t purchase unless you can pay it off before late fees kick in, and then make sure you keep your payments on time.

- Consider how expensive late fees would be. If you can’t make your payments in time to avoid these fees, you need to figure out whether they are actually cheaper than paying credit card interest would be.

If you use BNPL just for convenience and pay the money off quickly, it can be an effective tool as long as the monthly fee is not significant. However, if you don’t have a plan for prompt repayment, you may find BNPL could drawing you deeper in debt and paying a high price for it.

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.