What is a credit score?

A credit score is a 3-digit number used to rate your behavior with credit and debt. This number changes over time as you open and close credit accounts, use credit available to you and make payments. Lenders use your credit score when considering how risky it is to lend money to you.

Get your free credit score

Start today. The sooner you know your baseline score, the sooner you can start to build credit history.

By clicking on the button above, you agree to the Credit Sesame Terms of Use and Privacy Policy.

- ON THIS PAGE

- What is a credit score?

- What are the types of credit scores?

- How are credit scores calculated?

- How are credit scores and credit reports connected?

- Who uses my credit score?

- What are some benefits of having a credit score?

- Where can I find my credit score?

- When do credit scores typically get used?

- In a nutshell

Share this

What is a credit score?

The concept of a credit score may feel complicated, but in essence it looks simply at your payment history, amount of debt, how long you have had debt and how many recent applications you have made for credit accounts. Information about these items are reported to the three credit bureaus, Experian, TransUnion and Equifax, who compile your credit report. The information on your credit report is used to calculate your credit score.

Your three-digit credit score captures your experiences with credit and debt and can help you track changes in your financial history over time, from the very first debt you encounter—such as the credit card you opened in college—up to the present. Credit score is a powerful tool that signals to prospective lenders your ability to make payments in a timely manner.

This number is unique to you but publicly available under federal law to lenders considering you as a borrower. Your score can be a point of personal pride for good financial management and a point of public documentation. A credit score is an easy way to explain to another person or prospective lender that you can honor your commitment to make timely payments on outstanding debts. In turn, higher scores might lead a lender to extend interest rates lower than they would for consumers with less-favorable credit scores.

You can get your credit score as part of a request for a credit report or independently of a credit report. A comprehensive solution is to open a free Credit Sesame account. This provides you with fast access to everything you need to know about your credit history, including your credit score. It includes helpful supporting information that makes sense of your score and report.

What are the types of credit scores?

There are several different credit scores available to you as a consumer, lender-based scores and generic scores. Lender-based scores are maintained by companies that might consider lending money to you in the future. Common generic scores are the FICO Score and the VantageScore, and they are most widely known by the average consumer.

Often, people access their credit score by requesting it from one of the three credit bureaus—Equifax, Experian or TransUnion. You can also access this information in a single location via Credit Sesame.

An important note is that your credit score may differ from one report to the next, depending on which bureau lenders report to. Each of the credit bureaus compiles information about your financial history independently of the others. Some credit bureaus might have more information than others. It is possible that a credit report can contain inaccurate information. In this case, you can challenge the innacuracy and have it rectified. It is import to monitor your score regularly and take action if you see a sudden change that cannot be explained by your credit behavior.

Rather than focusing only on a single credit score, it’s a good idea to review as many sources as possible with information on your credit history. This gives you a better understanding of your financial health, including strengths and areas for improvement, as you plan future financial decisions.

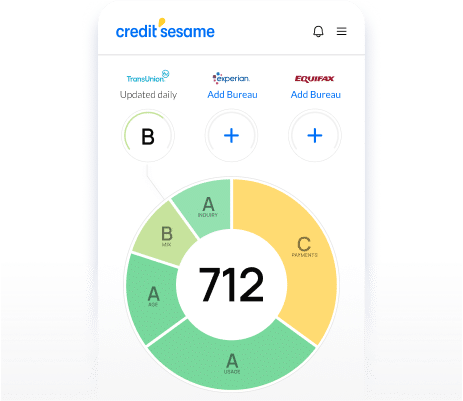

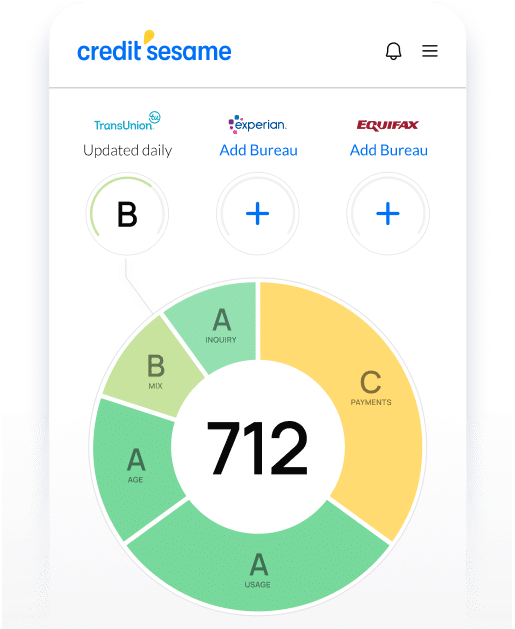

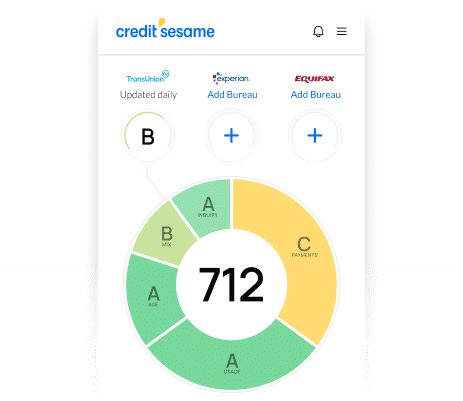

How are credit scores calculated?

Several factors influence your credit score for each of the two main credit scores:

Payment history

- 35% of your FICO Score

- 40% of your VantageScore

Credit age/depth of credit accounts

- 15% of your FICO Score

- 21% of your VantageScore

Credit utilization

- 30% of your FICO score

- 20% of your VantageScore

Credit account mix/balances

- 10% of your FICO Score

- 11% of your VantageScore

Credit enquiries/recent credit

- 10% of your FICO Score

- 5% of your VantageScore

Available credit

- 0% of your FICO Score

- 3% of your VantageScore

There are times when additional activity on your credit report can lead to a lower-than-expected credit score. For example, multiple applications for credit in a narrow window can reduce your score. Additionally, maxed out accounts and late payments can be problematic. Credit scoring organizations look favorably on consumers that use credit regularly without reaching their peak capacity. Reliable and responsible credit and financial behavior is another plus that can generate a higher credit score.

How are credit scores and credit reports connected?

A credit score summarizes the insights found in a credit report. A credit report is a detailed guide to your financial history including all types of debt—including credit cards, car loans, student loans, mortgages and more.

The activity found in a credit report, taken together, is used to calculate a score that reflects your overall credit risk to lenders.

Keep in mind that federal law does not require credit bureaus to report a credit score and, typically, your credit score is not included on your credit report. You might need to obtain your score separately from your free annual report. Alternately, Credit Sesame can provide your report and score in a single easy-to-access platform.

Who uses my credit score?

Legally, a variety of entities and people can request a copy of your credit report, which is the information that feeds into your credit score. According to the Consumer Financial Protection Bureau (CFPB), this list includes:

- Businesses to whom you owe money

- Government agencies

- Landlords

- Employers

- Insurance providers

- Banks and financial providers

- Legal entities (in the event of court orders, for example)

- Others you have authorized in writing to receive a copy

Although these people and organizations might never see your credit score—which can vary depending on who provides the score—they depend upon the information in your credit report to make decisions. For example, these entities might review your credit report to answer questions such as:

- Can I trust this person to pay their monthly rent on time and at the rate we’ve agreed upon?

- At what interest rate should I extend this bank loan to my client?

- Is this person eligible to participate in a state or federal government program I manage?

- Can I confirm this job candidate’s identity and confidently extend a job offer?

- Is this person in a position to pay the child support they owe?

Requests for credit reports are common and generally serve as a tool for verifying your information. They also help others make an informed decision about the terms and conditions for extending credit and working with you in other financial capacities in the future.

What are some benefits of having a credit score?

There are several positive reasons to have a credit score. A credit score serves as shorthand for your overall financial history. When you share your credit score with a trusted financial adviser or a prospective lender, they can immediately place you on the scale for that score—for example, somewhere between 300 and 850 in the case of the FICO Score.

Although this is a broad view, it enables the other party to arrive at some general impressions of your financial health. For example, a higher score could signal you have used debt wisely in the past. You have kept an appropriate balance of available credit and credit actively in use. You’ve made payments on time and avoided making too many requests for new credit.

A lower credit score might signal you have faced financial challenges. For example, perhaps you have maxed out some of your accounts. You might have lost a job or encountered other issues that led to missed payments.

The good news about a credit score is that it changes positively in response to good credit behavior. If you have a higher score, you can maintain and improve it with the right financial habits. If you have a lower score, you can focus on making timely payments and paying down balances you’ve had on file for some tim to increase your score. There are may ways to improve the building blocks of your credit report, which rolls into your credit score.

Where can I find my credit score?

Your credit score can be found in several places. One of the most common ways to get your score is to review your online or print statements from a credit card or a loan in your name. Increasingly, financial organizations are posting this information for your customers. Your lender is an example of a company that keeps your score on file.

Several types of nonprofit financial advisers can also help you access your credit report and corresponding credit score. For example, nonprofit credit counselors and even some federally approved housing counselors can support you in reviewing this information to get the answers you need.

A variety of credit score companies can help you get your credit score. Credit Sesame provides free accounts that enable you to access a summary of your credit report and credit score in one place.

Finally, a credit score can be purchased from the three credit reporting bureaus.

Make sure any credit score you obtain is the same kind of score that a lender would use to evaluate whether you are eligible for a loan. Some groups can provide you with an educational credit score. These aren’t preferred because often, they aren’t the same number that a financial institution would use to make a decision involving credit.

When do credit scores typically get used?

Credit scores get used by individual consumers who want to understand their own personal credit health. Scores might be reviewed when preparing for a major life decision, such as opening a business or starting college. A credit score can provide greater understanding of the terms likely to be offered by lenders for a loan or credit card.

At other times, credit scores might be used by another party such as a bank to determine whether to extend a loan. Lenders also use credit score as a factor in determining the interest rates and terms to apply. As credit score is not included in your credit report, it is a good idea to focus on taking steps that can improve your overall credit portfolio and credit report. These data points are available for others to access, and they contribute directly to your credit score.

In a nutshell

Credit scores are three-digit numbers that rate your historic use of credit and debit. They vary depending on the entity calculating the score but are broadly similar with 300 as the lowest score and 850 as the highest score. It is important for consumers to focus on maintaining good financial behavior as this impacts the underlying credit report used to calculate credit score.

Use your credit score as a measurement of your overall management of credit and debt, and focus your attention on steps that can improve your credit report—which contains the data that informs your score.

Do more with your FREE score™

Check your score right away and see the factors impacting your credit

By clicking on the button above, you agree to the Credit Sesame Terms of Use and Privacy Policy.

Share this

More related articles

Check your credit score for FREE

Checking your score to see where you stand is FREE and does not impact your credit.

See your score.

Reach your goals.

See your score. Reach your goals.

Begin your financial journey with Credit Sesame today.

Get your FREE credit score in seconds.

By clicking on the button above, you agree to the Credit Sesame Terms of Use and Privacy Policy.