You hear about a credit score this, and a credit score that all the time. Television, Radio, even the internet are telling you how important it is. But what is a credit score? This three digit number can have a huge impact on your financial health and can be the stepping stone needed to make major life purchases like a home, a car, and more. In this article, we’ll explain what a credit score is, how it is calculated, and why you should even care.

Why is your credit score important?

A credit score is essentially your credit history expressed as a three-digit number. You could also think of your credit score as a “grade” that shows how responsibly you’ve managed loans, credit cards, and other financial obligations over time. Generally speaking, credit scores range from 300 to 850 —the higher your score, the better your credit.

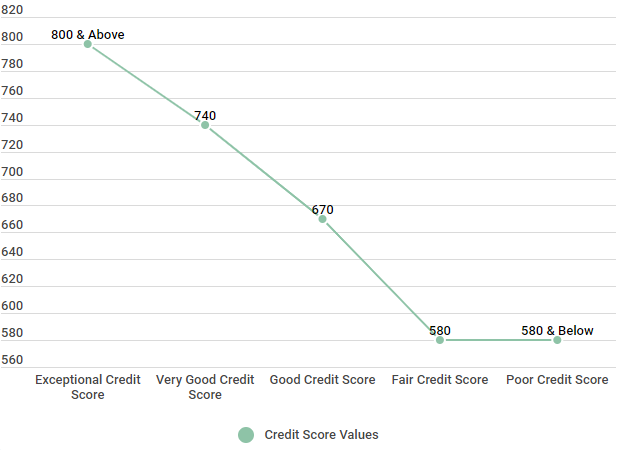

Here is a great reference chart that shows the different credit range breakdowns for the FICO score, the most commonly-used credit scoring formula.

FICO credit score ranges

| Credit Score Ranges | Credit Score Values |

|---|---|

| Exceptional Credit Score | 800 & Above |

| Very Good Credit Score | 740 - 799 |

| Good Credit Score | 670 - 739 |

| Fair Credit Score | 580 - 669 |

| Poor Credit Score | 580 & Below |

Source: Fair Isaac Corporation (myFICO.com).

The information used to calculate your credit score (such as your payment history) is provided by your creditors to different credit bureaus. The three credit bureaus are TransUnion, Equifax, and Experian.

When you apply for a mortgage or car loan, your credit score is used to determine whether or not the lender 1) believes that you are a risk worth taking and 2) what the interest rate and terms will be based on your creditworthiness.

| Free credit score |

|---|

| What's a credit score |

| What is a fico score |

| Building credit |

| Average credit score by age |

| Perfect credit score |

Why is a credit score important?

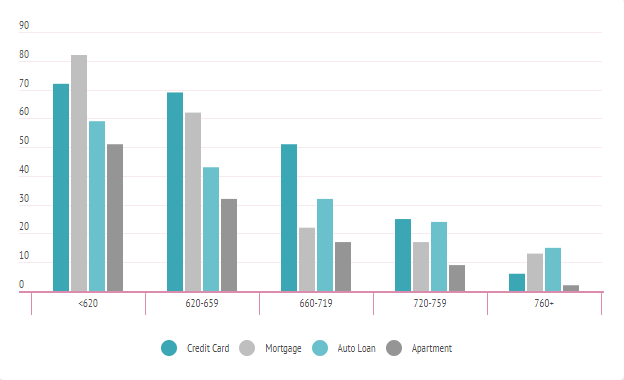

As you can see from the data below, the lower your credit score, the more likely you are to get denied for a loan or purchase. In this particular study, we looked at consumers who had been turned down because of their credit score for various purchases. Those with credit scores of less than 620 were rejected far more than those with 720 or higher scores.

Americans who are Denied Due to Credit Score

| Credit Score | Credit Card | Mortgage | Auto Loan | Apartment |

|---|---|---|---|---|

| <620 | 72% | 82% | 59% | 51% |

| 620-659 | 69% | 62% | 43% | 32% |

| 660-719 | 51% | 22% | 32% | 17% |

| 720-759 | 25% | 17% | 24% | 9% |

| 760+ | 6% | 13% | 15% | 2% |

Source: Survey of 2000 members and non-members who had been turned down on a credit application within the last quarter. Survey done on 5/5/2018.

Even those with excellent credit can be denied a loan, but the rates increase as your credit score decreases. Being rejected for a car loan or a credit card may not seem like that big of a deal. However, there are some major implications should you be approved.

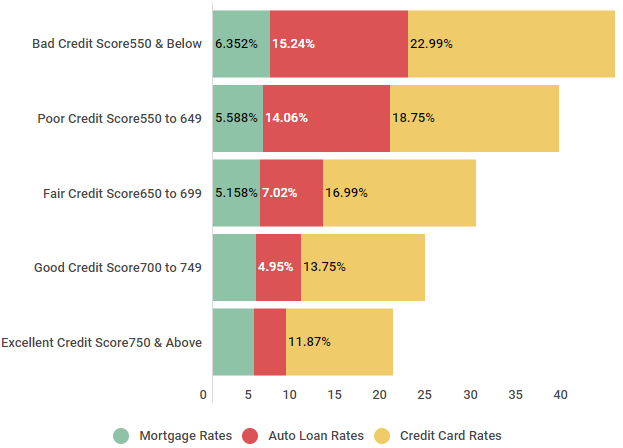

As you can see from the data below, interest rates fluctuate greatly depending on your credit score. When you consider the costs associated with carrying a higher interest rate over the term of a 30-year loan or a 3-year auto loan, the dollars can quickly add up.

Comparing Interest Rates Based on Credit Score Range

| Score Range | Mortgage Rates | Auto Loan Rates | Credit Card Rates |

|---|---|---|---|

| Bad Credit Score 550 & Below | 6.352% | 15.24% | 22.99% |

| Poor Credit Score 550 to 649 | 5.588% | 14.06% | 18.75% |

| Fair Credit Score 650 to 699 | 5.158% | 7.02% | 16.99% |

| Good Credit Score 700 to 749 | 4.767% | 4.95% | 13.75% |

| Excellent Credit Score 750 & Above | 4.545% | 3.60% | 11.87% |

Source: Credit scores were calculated from 5,000 Credit Sesame members on 3/11/18.

While 2 percent does not seem like that much on first look, over 30 years that could mean more than $100,000 difference in interest fees. Imagine what you could do with that extra money, by just increasing your credit score a small amount.

Guide to your credit score

Once you’ve started to learn more about your credit score, you’ll realize that “credit score” is a pretty generic term. Believe it or not, we each have many different credit scores. However, the two most widely used credit scoring models are the FICO score and the VantageScore. While each of these have their own method for calculating your score, the factors that they look at remain largely the same for both.

Understanding these factors and how they impact your score is the first step in understanding the meaning of your score.

Calculating your credit score

As we mentioned before, your credit score is based on the information contained in your credit report and is a numerical representation of your credit history.

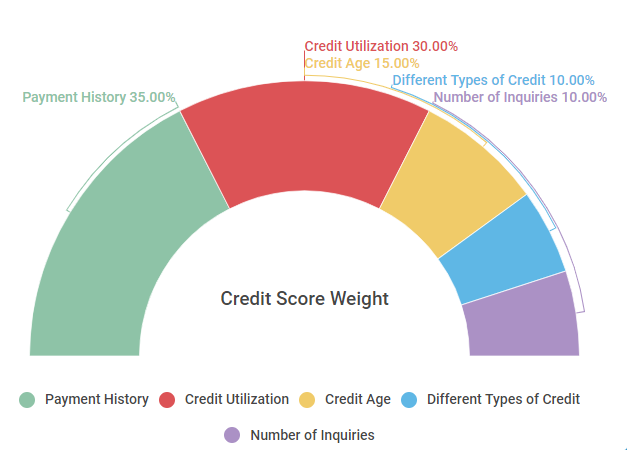

As you can see from the chart below, the FICO scoring model weighs several different factors when calculating your score. They include things like your payment history, the age of your credit, the number of inquiries you have, and more.

FICO Scoring Model Calculation (Weight) Factors

| Credit Factors | Credit Score Weight |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Different Types of Credit | 10% |

| Number of Inquiries | 10% |

Source: Data found September 26, 2018. Boeing Employees Credit Union website. Understanding Your FICO Score. Retrieved from https://www.becu.org/articles/understanding-your-fico-score

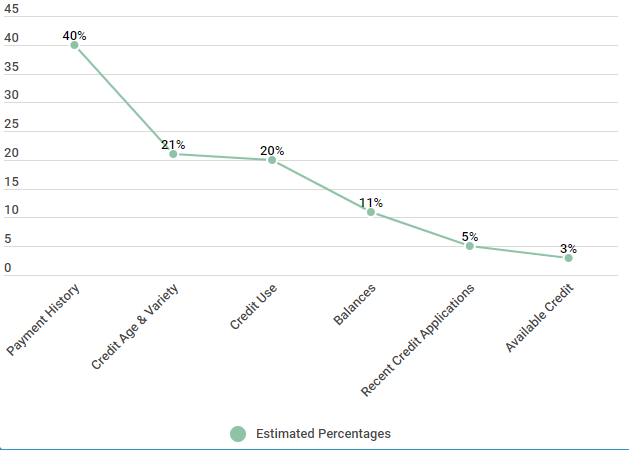

Similarly, the VantageScore scoring model takes several factors into consideration when calculating your score. As you’ll see below, they are quite similar to those used by FICO but are weighted a bit differently.

VantageScore 3.0

| VantageScore Factors | Estimated Percentages |

|---|---|

| Payment History | 40% |

| Credit Age & Variety | 21% |

| Credit Use | 20% |

| Balances | 11% |

| Recent Credit Applications | 5% |

| Available Credit | 3% |

Source: Data found October 3, 2018. Your VantageScore website. (2017) VantageScore 4.0 Overview. (PDF file.) Retrieved from VantageScore 4.0 Overview. (2017). 1st ed. [ebook] VantageScore, p.4. Available at:

https://your.vantagescore.com/images/resources/VS4%20Overview%20WP%20-%20FNL.pdf [Accessed 3 Oct. 2018].

Let’s look at each of these factors means and how they impact your score. Because FICO is the most widely used, we’ll look at their calculation factors.

Payment history

Your payment history is the single most important factor when calculating your credit score; it accounts for roughly 35% with Fico and 40% with VantageScore. But it’s not just whether or not you pay on-time.

Other items that go into your payment history include:

- The number of credit accounts and loan accounts that you have paid on time

- The number of accounts on which you are currently 30-days or more behind on your payments

- Whether or not you have declared bankruptcy

- Whether or not you have had any accounts turned over to collections

- How many days past due you are on any delinquent accounts

- The total dollar amount past due on any delinquent accounts or those sent to collections

As you can see from the data below, a 30-day late payment can cause a 25 point drop in your score, and that drop in score goes up the longer you don’t pay the bill.

Late Payment Delay & Credit Score Drop

| Late Payment (Days) | Average Credit Score Drop (TransUnion) | Average Credit Score Recovery (TransUnion) in 6 Months |

|---|---|---|

| 30 Days | 25 Points | 85 Points |

| 60 Days | 45 Points | 65 Points |

| 90 Days | 65 Points | 40 Points |

| 150 Days | 100 Points | 35 Points |

| Charge Off | 150 Points | 20 Points |

Source: We tracked a group of 500 members targeting those who have missed payments on their loans for different amounts of time and how much their credit score dropped during those time frames.

You can also see that the score recovery, the amount the score rebounded when the bill was paid is not always equal to the initial score drop.

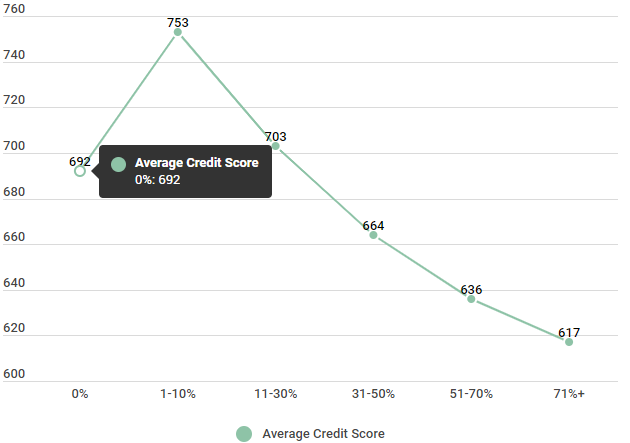

Credit utilization

Not only is the total dollar amount that you owe important, but the percentage of your available credit you are using is also important. Your credit utilization looks at the total available credit you have versus your total debts. Most experts agree that you should keep this number below 30%, with the ideal ratio being around 10%.

Your credit utilization also looks at:

- The number of accounts you currently have a balance on

- Your total credit utilization

- The amount you own on existing accounts and loans

The data below suggests that credit utilization has a direct impact on your score —and it should. FICO weighs your credit utilization as roughly 30% of your score.

Impact of Credit Utilization on your Credit Score

| Credit Utilization | Average Credit Score |

|---|---|

| 0% | 692 |

| 1-10% | 753 |

| 11-30% | 703 |

| 31-50% | 664 |

| 51-70% | 636 |

| 71%+ | 617 |

Source: https://www.newyorkfed.org/microeconomics/databank.html

As you can see, as the credit utilization reached that sweet spot of 1-10%, scores were their highest. It should be noted that using none of your available credit can, perhaps surprisingly, have a negative impact.

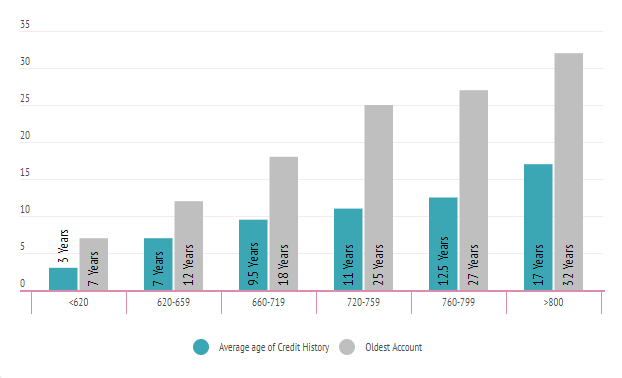

Credit history

Another important factor that lenders will consider when deciding whether or not to extend you credit is a long-standing history of credit use. How long you’ve been actively utilizing your credit can provide lenders a glimpse into your spending habits and financial health.

Your credit history is typically determined by looking at the age of your oldest account, or the average age of your open accounts —rather than when you first used credit.

Average Age of Credit History

| Credit Score Range | Average age of Credit History | Oldest Account |

|---|---|---|

| <620 | 3 Years | 7 Years |

| 620-659 | 7 Years | 12 Years |

| 660-719 | 9.5 Years | 18 Years |

| 720-759 | 11 Years | 25 Years |

| 760-799 | 12.5 Years | 27 Years |

| >800 | 17 Years | 32 Years |

Source: Credit Sesame surveyed 510 adults from July 14, 2018 to July 20, 2018.

As you can see from the data above, those with the highest credit scores also have the longest history of credit usage.

Types of credit utilized

Another factor that many people tend to forget is the types of credit you utilize. This factor looks at how many different types of credit accounts you’ve used, as well as how recently you’ve used them.

A good mix of credit can include credit cards, store cards, mortgage loans, auto loans, and others. Typically, showing responsible use of more than one type of credit indicates that you are a well-rounded borrower.

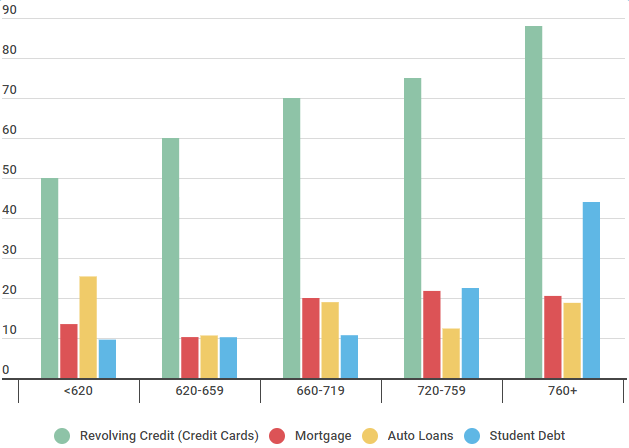

Types of Credit utilized by Credit Score Range

| Types of Credit Utilized | Revolving Credit (Credit Cards) | Mortgage | Auto Loans | Student Debt |

|---|---|---|---|---|

| <620 | 50% | 13.48% | 25.39% | 9.6% |

| 620-659 | 60% | 10.23% | 10.63% | 10.2% |

| 660-719 | 70% | 20% | 18.96% | 10.7% |

| 720-759 | 75% | 21.77% | 12.37% | 22.5% |

| 760+ | 88% | 20.52% | 18.79% | 44% |

Source: https://www.newyorkfed.org/microeconomics/databank.html

The chart above shows the types of credit compared to the credit score of consumers. As you can see, there’s a wide mix here of various loan types —which correlates to better credit scores.

New credit

The final piece of the credit score puzzle includes your new and/or recent credit. Here, lenders are looking for this information to show your recent financial performance —to use it as an indicator of how you will handle your accounts moving forward.

This credit scoring factor looks at how many loans or lines of credit you’ve opened recently, how long it’s been since you opened your last account, the number of inquiries you’ve had into your credit report, and how long it’s been since you had an inquiry.

While this may seem like information that’s not very important, too many inquiries can be a big red flag for lenders.

We recently spoke with Tyler who applied for several credit accounts in a short period of time. Here is his story.

Tyler applied for new credit and is now regretting it.

Member Since: 3/4/2017

We interviewed Tyler on August 5, 2018. Tyler is a 23-year-old mechanic who lives in Peekskill, New York. His girlfriend Sandra is in college in New York City.

| Please | share | a | time | when | new | or | recent | credit | impacted | your | credit | score. |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| I have had a truck for the last three years and I wanted to put a new stereo in it. Because I didn’t have enough money to buy it outright I financed it. It looked good, and I barely read the agreement and so when I checked my Credit Score the following week, I was shocked. I hadn’t realized that my credit would be requested. Looking back at it, I should have known. | ||||||||||||

| What | sort | of | change | did | you | see? | ||||||

| It went down over 20 points. I couldn’t believe that my Credit Score could go down that far from just one inquiry. | ||||||||||||

| What | were | the | circumstances | surrounding | the | inquiry? | ||||||

| I was initially really upset but when I looked at my Credit Report I noticed that this wasn’t the first time that my credit had been requested in the last 30 days. A week before I bought the stereo, I had rented a new apartment. A week before that I had applied for a new credit card. Those three things, all different, really affected my credit score. | ||||||||||||

| Looking back, what would you have done differently? | ||||||||||||

| I would have still rented the apartment, but I do not think I would have bought the stereo or applied for the credit card. I can do without a new stereo, since my truck already has one in it. I got the credit card so I could buy a plane ticket to North Carolina to see family. Looking back on it, I could have just saved a little every month and I would have still been able to travel and my Credit Score would not be so low. |

Tyler’s story is a great reminder that we need to really understand the meaning of our credit score, how it’s calculated, and the things that we do on a daily basis that can impact it.

Benefits of learning the meaning of your credit score

At the end of the day, learning about the meaning of your credit score is important for a number of reasons —but primarily because knowledge is power. When you are armed with a solid knowledge of how your credit score is calculated and how it works, you can make adjustments to make sure your score is always improving.

And, if you’re thinking about improving your score, you’re not alone. As you can see, a whopping 83% of Millennials are actively trying to improve their credit score —and they’re not the only generation working on their scores.

Who’s Actively Improving Their Credit Score

| Age | Improving (2014) | Improving (2015) | Improving (2016) | Improving (2017) |

|---|---|---|---|---|

| Gen Z (up to age 23) | 67% | 69% | 71% | 72% |

| Millennials (23-34) | 73% | 77% | 81% | 83% |

| Generation X (35-54) | 70% | 69% | 67% | 66% |

| Baby Boomers (55+) | 38% | 36% | 36% | 34% |

Source: Credit Sesame surveyed 510 adults from July 14, 2018 to July 20, 2018.

We’ve created a wealth of great content containing strategies to improve your score. So, if you’re just learning about credit scores, and how important they are, here is a good article about improving your credit.

TLDR; why your credit score matters

To recap, your credit score is a three-digit number that is calculated based on your credit history. There are varying formulas for that calculation, but most look at a variety of similar factors like your payment history, your credit utilization, your applications for new credit, and more. Lenders use this information to determine if they want to lend to you and, if so, the interest rates and terms associated with that loan.

Knowing the meaning of your credit score and how it’s calculated is the first step in taking charge of your financial health and, if needed, making adequate steps to improve it.