Table of Contents

- Introduction

- How Long Does it Take to Build Credit?

- Steps to Improve Your Credit Score

- Cautiously Pay Off Debt

- Keep Credit Card Balances Low

- Leverage Mortgage/Car/Utility/Cell Phone Payments

- Check Your Free Credit Reports for Mistakes

- Increase Your Credit Limit

- Steps to Improve Credit Over the Long-Term

- Improve your Credit Utilization

- Maintain a Healthy Credit Mix

- Pay Your Bills on Time

- Leverage Mortgage/Car/Utility/Cell Phone Payments

- Apply for and Open New Credit Accounts Only as Needed

- Don’t Close Unused Credit Card Accounts

- Avoid Applying for a Ton of Credit Products

- Credit Score FAQ

- What Is a Credit Score?

- Why is Your Credit Score Important?

- Benefits of a Good Credit Score

- What Is the Average Credit Score by Age?

The major credit score factors are:

- Payment History (Credit History)

- Credit Utilization

- Credit Age

- Different Types of Credit (Credit Mix)

- Number of Inquiries

Each of these factors plays a role in your path to credit score improvement. The first two generally make up 65% of your total credit score weight so make sure you are paying your bills on time and keeping your credit utilization below 30%, or better yet, 10%, and you should start seeing your credit improve over time.

If you’re ready to get started on the road to improving your credit score, you can get a personalized free credit report summary from Credit Sesame and know your baseline numbers today.

Introduction

Goodbye, 2020! As we shake off the year that everyone will be happy to leave in the past, there’s no better time than now to look towards a positive future.

Good credit history in general translates to a major part of a successful financial future. A positive score can open doors to jobs, apartments, even the ability to turn on your utilities.

In this article, you’re going to learn ways to improve your credit score as fast as you possibly can, but please remember that this can still take some time. There are no guarantees as this is all dependent on your specific situation.

How Long Does it Take to Rebuild Credit?

It largely depends on the negative information (i.e. late payments, bankruptcy, too many inquiries, etc.) that exists on your credit report. It can take as little as 1 month, and take as long as 12 months or more. It all depends on your previous and future activities.

The length of time improvement takes can depend on the reasons behind the negative marks inflicted on your credit score, such as a delinquency or collection account. These unfortunately will stay with you until they reach a certain age.

- Inquiries remain on your report for up to 2 years

- Delinquencies will last up to 7 years

- Bankruptcies can last 7-10 years

Rebuilding your credit and improving your credit scores takes time; and unfortunately there aren’t any shortcuts you can take. All you can do is clean up the other items that are within your control, which we’ve laid out in this article.

Steps to Improve Your Credit Score

As previously mentioned – there is no ‘quick fix’ for bad credit scores, but there are certain things within your control that you can start working on today. Below are the primary ways to improve your credit score:

1. Cautiously Pay Off Debt

Paying off your outstanding collections debt will help … right? Not necessarily and we will explain more below. Sometimes it simply resets the clock and dings your history even harder. Three things to know here:

- The newest versions of FICO® and VantageScore® ignore paid collections

- Pay off the most recent delinquent accounts first because these hurt your score the most

- Non-medical collection debt hurts your score more than medical collections

Fixing unpaid collections can be another major component of improving your score. However, proceed with caution here as paying down some accounts in collection will not always improve your score but can actually reset the clock on how long it will take for that debt to fall off your report. Do your research.

2. Keep Credit Card Balances Low

Your credit utilization ratio generally counts nearly as much as payment history. Credit utilization is the amount of total debt versus total credit limit. Very high credit utilization, or amounts owed, means that your credit cards may be maxed out or close. For example, if you’re carrying $3,000 in debt with a $4,000 combined credit limit, your credit utilization ratio is 75 percent.

The solution: bring down your balances. The lower your ratio, the better the boost. People with the highest credit scores typically use no more than 10 percent of their available credit.

Credit utilization is calculated for each credit card as well as for an overall tally. Even one tapped-out credit card can hurt your score.

3. Check Your Free Credit Reports for Mistakes

Nothing is flawless. Mistakes happen. Error correction is the simplest way to improve your score. According to the Federal Trade Commission, one out of five consumers has an error on at least one of their credit reports. Don’t let misreported information be the cause of poor credit when it’s relatively easy to fix.

Regularly checking your credit score is an essential first step toward improving your score. How can you bring up the number if you don’t know what it is? As you can see from the chart below, those who check their score on a regular basis see the benefits.

4. Increase Your Credit Limit

By its nature, contacting banks to request increases on the credit limits for your cards would decrease your credit utilization ratio, provided you don’t increase your spending habits as well.

This can be a great credit score optimization strategy to employ, since it will benefit you regardless of your current credit score. Even those with excellent credit can see a slight bump in their score by increasing their credit limits and acting responsibly with those increases.

Steps to Improve Credit Over the Long-Term

1. Improve Your Credit Utilization

You can’t max out your credit cards and still have a good credit score. You need to keep your ratios low. One of our philosophies is that you should only make purchases on your credit card (emergencies are an exception) when you can pay for them out of pocket.

Improving your credit utilization is the second most important step toward improving your credit profile. Successful credit applicants and those with the highest scores generally have the lowest percentage of credit utilization in relation to the total amount of credit they have.

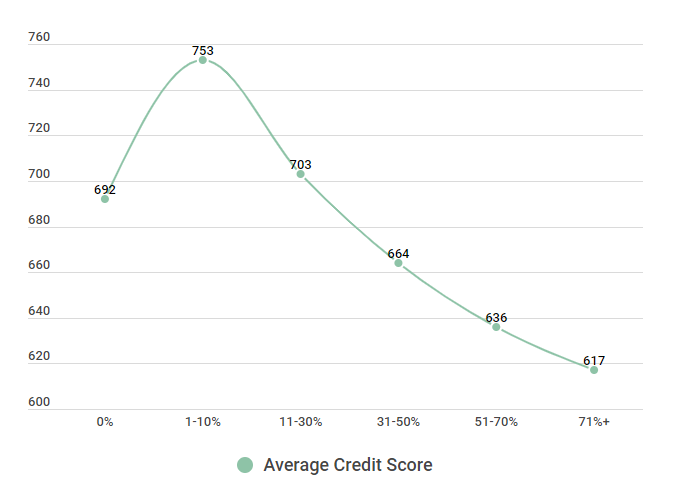

Impact of Credit Utilization on your Credit Score

| Credit Utilization | Average Credit Score |

|---|---|

| 0% | 692 |

| 1-10% | 753 |

| 11-30% | 703 |

| 31-50% | 664 |

| 51-70% | 636 |

| 71% | 617 |

Source: https://www.newyorkfed.org/microeconomics/databank.html

The pattern here is quite clear – don’t overuse your credit or you’ll risk lowering your credit score quite significantly. Just compare those who have an average of 1-10% utilization and a 753 credit score compared to those with 51-70% and a 636 credit score.

Being able to apply for new credit or loans will become a lot more difficult once you find yourself in the average or poor credit score range.

2. Maintain a Healthy Credit Mix

The credit bureaus want to see evidence that you can successfully manage a variety of credit types. For example, student loans, mortgages, and auto loans are all installment loans with a fixed payment, but a credit card or home equity line of credit represents a revolving credit with variable payments.

Lenders want to know that you can handle different types of credit products, and look favorably on those who have several credit accounts open. However, be careful about opening too many new accounts at once. Lenders view multiple applications for credit cards negatively.

Credit Mix & Resulting Change Timeframe

Types of Credit (open, unsecured, secured, revolving, installment) |

Typical Impact to Score |

How Long It Takes to See Changes |

Two Types |

10 – 15 Points |

1 – 2 Months |

Three Types |

10 – 15 Points |

1 – 2 Months |

Four Types |

15 – 20 Points |

1 – 2 Months |

Five Types |

12 – 20 Points |

1 – 2 Months |

Source: Survey was conducted by Credit Sesame on 02/13/18 with a total of 500 responses.

Although credit mix doesn’t have the greatest amount of weight for improving your credit score – improving the different types of credit you have can give you a decent boost to your credit standing.

Average Time to See Credit Score Improvement (Credit Mix Impact)

Credit Score Factors |

0-3 Months |

3-6 Months |

6-12 Months |

12+ Months |

Payment History |

+20 Points |

+36 Points |

+48 Points |

+60 Points |

Credit Utilization |

+15 Points |

+29 Points |

+41 Points |

+55 Points |

Length of Credit History |

+5 Points |

+7 Points |

+12 Points |

+20 Points |

Credit Mix |

+10 Points |

+11 Points |

+12 Points |

+14 Points |

New Credit |

+10 Points |

+9 Points |

+7 Points |

+6 Points |

Source: Survey of 750 Credit Sesame members who actively worked on improving their credit score by following the personalized tips in the Credit Sesame app. Survey completed over the course of 24 months from 2/15/2016 – 2/15/2018.

3. Pay Your Bills on Time

The number one factor in your score is your payment history. Late payments can quickly drop your credit score. Each payment helps, but just one missed payment can wreck that progress. If you miss a due date, make the payment as soon as possible since lenders typically don’t report a payment late until 30 days after it is due.

Since this generally accounts for about 35 percent of your score, you can’t afford to ignore it. Instead, make bill payment a priority. If you need to make a schedule, do it. If you need a dedicated calendar for the purpose, go for it. Whatever it takes to get yourself on a strict payment schedule, that’s what needs to happen.

4. Leverage Mortgage/Car/Utility/Cell Phone Payments

Paying your bills on time, every time, can help to rebuild your credit score. Instead of paying your bills, such as your mortgage, car loan, utilities and cell phone, with your checking account or cash, we suggest paying by credit card so that the credit bureaus have record of your timely payments.

Unlike a small business, individuals cannot self-report to the three major credit report companies. However, there are third-party services that can report the information on your behalf. But you may not need to do that if you pay on time every time with a credit card. Your credit card companies will automatically send that information to the credit bureaus within 45-60 days for your credit report.

5. Apply for and Open New Credit Accounts Only as Needed

When you apply for a new credit card, you will most likely activate a hard inquiry – also called a hard pull. Hard inquiries show up on your credit report and can cause your credit score to take a hit. For example, four hard inquiries in a 90-day period could lower your credit score by 50 points. Hard inquiries can also stay on your credit report for two years.

Additionally, lenders may get concerned if they see multiple hard inquiries on a credit report and may consider you as a high risk borrower. You should avoid applying for multiple cards simultaneously and/or within a short time frame. A good rule of thumb is to wait about six months after applying for a line of credit before applying for another.

6. Don’t Close Unused Credit Card Accounts

While it may sound counterintuitive to keep unused credit cards, in general, you shouldn’t close them just because they’re unused. Older cards show the lender that you have a longer credit history. This becomes important if you are applying for a mortgage or any other type of loan.

Credit age generally accounts for about 15% of your credit score. Since you’ll gain points in this category over time, you generally shouldn’t close old accounts or those you have paid off.

Also, if you close a credit card account, your credit utilization may increase, which could lower your credit score.

7. Avoid Applying for a Ton of Credit Products

Each inquiry into your credit, which is what happens with each credit application, can drop your score by a few points. Soft inquiries–which include employment checks, self-checks, and inquiries to prequalify you for promotional offers–do not hurt your score. Hard inquiries are those made as the result of an application for new credit. Hard inquiries are the inquiries you should strive to limit in a short timeframe as discussed above.

Credit Score FAQ

What Is a Credit Score?

A credit score is a number generally ranging from 300-850, as assigned by one or all of the three credit bureaus, that depicts a consumer’s credit rating and is largely derived from the consumer’s credit history, such as their: total amount of debt, history of repaying loans, number of open accounts, etc. The higher the credit score, the more attractive it is to lenders. Lenders use credit scores to evaluate the probability that an individual will repay loans in a timely manner.

As you can see from the chart below, payment history is the single most important factor when it comes to your FICO credit score. After that comes credit utilization, and the two together make up the bulk of your score. That’s not to say you should ignore the other factors at work, but understand that these are the major players here. The factor weights, while can vary, are generally the same for Vantage and Experian scores.

FICO Scoring Model Calculation (Weight) Factors

Credit Factors |

Credit Score Weight |

Payment History |

35% |

Credit Utilization |

30% |

Credit Age |

15% |

Different Types of Credit |

10% |

Number of Inquiries |

10% |

Source: Data retrieved from https://www.myfico.com/credit-education/whats-in-your-credit-score

Why is Your Credit Score Important?

When it comes to improving your credit, there really is no time to waste. A low credit score may not seem like a big deal until it’s time to leverage your credit for a car loan, mortgage, insurance, and many other big life events. Americans with low credit scores may not be eligible to borrow money for these things and/or might end up with much higher interest rates than someone with a higher credit score. The earlier you begin working to build and improve your credit score, the easier it will be for you to accomplish these things.

Benefits of a Good Credit Score

The higher your score, the lower your interest rates will generally be and the easier it will be for you to obtain credit which will open up more opportunities for you to reach your financial goals. And the lower your credit score, the harder it is to get low insurance rates, qualify for credit cards, and more. Do more with your credit score.