When you use your credit card, it has a direct influence on your credit score. In fact, both the FICO score and the VantageScore models weigh your payment history and your credit utilization the most when calculating your score. Because of this, if you’re trying to rebuild your credit, using credit cards responsibly can be one of the quickest and most effective ways to see improvement.

Introduction

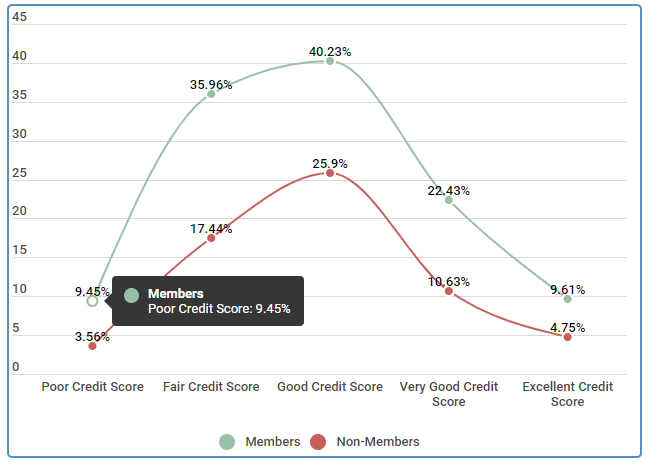

If you’re trying to rebuild your credit, you’re not alone. As you’ll see from the data below, the percentage of people actively working to improve their credit score is increasing in many credit score ranges. In fact, a 40 percent of individuals with good credit scores say that they were working to improve their credit in 2018.

Percent of Americans Actively Working to Improve Their Credit Score

| Actively trying to repair | Members | Non-Members |

|---|---|---|

| Poor Credit Score | 9.45% | 3.56% |

| Fair Credit Score | 35.96% | 17.44% |

| Good Credit Score | 40.23% | 25.9% |

| Very Good Credit Score | 22.43% | 10.63% |

| Excellent Credit Score | 9.61% | 4.75% |

Source: Survey of 1000 members and non-members who have a credit score.

Why is this happening? We’ve all heard about the importance of our credit score. It is what lenders look at when deciding whether or not to extend you credit for things like mortgages, car loans, and credit cards. The better your score, the more favorable the interest rate you’re able to receive.

But, your credit score is also related to other life milestones like getting your first apartment and the amount of deposit you’ll be asked for, setting up the utilities for that apartment (and the deposits you’ll pay there, too), as well as getting a cell phone contract, car insurance, and more.

| Related to " Rebuild Credit Using Credit Cards" |

|---|

| Free Credit Score |

| What is a Good Credit Score |

| How to Improve Your Credit Score |

| How to Build Credit |

| How to Fix Your Credit |

| Perfect Credit Score |

Why you should know how to rebuild your credit using credit cards

Your FICO credit score, the most widely used and accepted scoring model, is calculated using a variety of factors. It is this score that helps lenders determine whether or not to extend you credit and what the accompanying interest rate may be. It’s important to understand how your score is calculated in order to make strategic steps that are able to improve your score —like rebuilding your credit with credit cards.

Here are the credit factors that are taken into consideration and how much importance are placed on each when calculating your score:

FICO Scoring Model Calculation (Weight) Factors

| Credit Factors | Credit Score Weight |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Different Types of Credit | 10% |

| Number of Inquiries | 10% |

Source: Data found September 26, 2018. Boeing Employees Credit Union website. Understanding Your FICO Score. Retrieved from https://www.becu.org/articles/understanding-your-fico-score

As you can see, payment history and credit utilization (both of which are directly related to your credit card usage) make up the majority of your score.

Here are some quick definitions to help you understand these various factors:

- Payment History—this is your history of paying on-time and includes any missed or late payments.

- Credit Utilization—this looks at the amount of credit you’re using (the balance of your accounts) vs. your available credit limit. The best practice is to keep the ratio under 30%.

- Credit Age —this looks at the average age of all your open credit accounts.

- Types of Credit—this looks at the mixture of credit types you have open like credit cards vs. mortgage accounts.

- Number of Inquiries—this looks at the number of times lenders have pulled your credit information. It’s best to keep this number as low as possible.

If you have questions about how to best increase your credit score using credit cards, you’re not alone. Here are just a few of the questions that Credit Sesame members had when starting to explore this topic:

| Increasing | Credit | Limit | to | Increase | Credit | Scores |

|---|---|---|---|---|---|---|

| Q How does increasing your credit limit help your credit? | ||||||

| A Increasing your credit limit helps your credit score by reducing your overall credit utilization. FICO states that credit utilization is responsible for 30% of your credit score. If consumers keep their credit utilization under 10% they are more likely to have a higher credit score than someone with credit utilization at, or above 30% total utilization. | ||||||

| Q Is adding another credit card the same as increasing the limit on my current credit card? | ||||||

| A No, adding another credit card has both advantages and disadvantages. These factors depend on how many inquiries are made into your credit history, the credit limit and whether or not you keep a high balance, and how often the creditors report your activity. Increasing the limit on your current credit card won’t require any credit checks and will automatically decrease your credit utilization ratio. |

If you’re ready to improve or rebuild your credit using credit cards, let’s look at the answers to these questions and the steps you can take to get started!

How to rebuild your credit using credit cards

Now that we’ve established a basic understanding of how your credit score is calculated and why it’s so important to have a good credit score, the strategies for rebuilding your credit score with credit cards will make more sense. Let’s look at some of these strategies:

Check your credit report

The very first step to rebuilding your credit is to check your credit report. Knowing your current credit standing will give you the best picture of where you’re starting from —and where you’d like to go. Each of the three main credit bureaus —Equifax, Experian, and TransUnion— are required to provide you with one free credit report per year.

Here’s a quick list of things you should look for:

- Any accounts that aren’t yours

- Any inquiries into your credit that you didn’t authorize

- Any errors to your address and employer

- Any account history (late payments, etc.) that aren’t correct

- Any open accounts you have that haven’t reported

- Any delinquencies, collections, bankruptcies that are not accurate

If you find an error on your report, you can file a dispute with the bureau to have it cleared up.

Make all payments on time

Once you’ve cleared your credit report of any errors, you can focus on best-practices using credit cards that will help improve your situation. Making all your payments on time may seem like a given, but it is one of the most important steps to improving your credit. Remember: payment history makes up 35 percent of your FICO score.

As you can see from the data below, having on-time payments can increase your score as much as 22 points in just 12 months.

Average Credit Score Improvement for On-Time Payments

| Credit Starting Point | 3 Months | 6 Months | 12 Months |

|---|---|---|---|

| Bad (550<) | +6 | +9 | +22 |

| Poor (550+) | +5 | +9 | +19 |

| Fair (600+) | +3 | +8 | +17 |

| Good (650+) | +3 | +7 | +14 |

| Very Good (750+) | +2 | +5 | +7 |

| Excellent (800+) | +2 | +3 | +5 |

Source: Review of 600 individuals who for the course of a year made all payments on time. The study was conducted in February of 2016 and concluded April of 2016.

If you have a hard time making on-time payments, there are some simple solutions you can try to help make the process easier:

- Set up calendar reminders on your phone a week before your payment is due so you’re reminded and have time to take action.

- Sign-up for automatic payments.

- If the creditor doesn’t have a system for automatic payments, create an automatic “bill pay” with your bank so they can send the payment directly and automatically.

Lower your credit utilization

As you may remember from the data above, your credit utilization makes up 30% of your FICO score. It looks at how much of your available credit you’re using. If you have a total credit limit across your different accounts of $10,000 and your balances are $4,000, then your credit utilization is 40%.

Most experts recommend having a credit utilization below 30%, although people with credit utilization below 10% are more likely to have a higher score.

As you can see from the data below, there is a direct correlation between lowering your credit utilization and increasing your score.

Average Credit Score Improvement from Lowering Credit Utilization

| Credit Ranking | Low Credit Utilization 10%< | Moderate Credit Utilization 30%< | High Credit Utilization 31%< |

|---|---|---|---|

| Excellent (800+) | +1% | +1% | -7% |

| Very Good (750+) | +1.8% | +2.5% | -6.5% |

| Good (700+) | +3% | +3.25% | -5% |

| Fair (650+) | +4.5% | +6% | -4.25% |

| Poor (600+) | +6% | +7% | -2.5% |

| Bad (550<) | +10% | +12% | -2% |

Source: Credit Sesame surveyed 600 Americans on how credit utilization impacts their credit scores. Groups were divided by Credit Rank (Bad, Poor, Fair, Good, Very Good, and Excellent) and then subdivided by Low Credit Utilization, Moderate Credit Utilization, and High Credit Utilization. The study took place October 2015 until November of 2016.

Using credit cards can help you improve your credit utilization in three main ways:

- You can pay off a portion of your credit card to help you improve your utilization to under 30%

- You can ask your existing credit card to increase your credit limit, which will improve your credit utilization.

- You can add a new credit card, which will increase your available credit and, therefore, improve your credit utilization.

Once you improve your credit utilization, it’s important to monitor it and make an effort to keep it in that sweet spot between 10 and 30%.

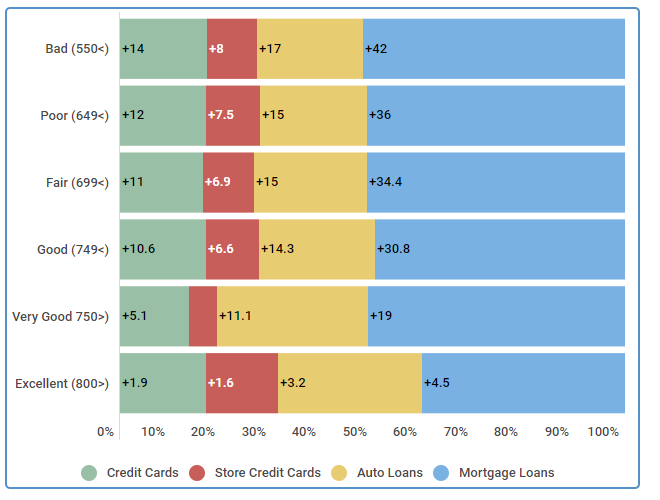

Diversify your credit mix

Another key component in the calculation of your credit score is your credit mix —or the variety of different types of credit you have. This can include credit cards, store credit cards, auto loans, student loans, mortgage loans, and others.

Lenders look for a credit profile that contains a variety of credit types, which demonstrates your ability to handle (and repay) different types of loans. As you can see from the data below, the most impact on a credit score was made by adding a mortgage loan.

Credit Score Improvements Gained by Diversifying Credit Account

| Credit Ranking | Credit Cards | Store Credit Cards | Auto Loans | Mortgage Loans |

|---|---|---|---|---|

| Bad (550<) | +14 | +8 | +17 | +42 |

| Poor (649<) | +12 | +7.5 | +15 | +36 |

| Fair (699<) | +11 | +6.9 | +15 | +34.4 |

| Good (749<) | +10.6 | +6.6 | +14.3 | +30.8 |

| Very Good 750>) | +5.1 | +2.1 | +11.1 | +19 |

| Excellent (800>) | +1.9 | +1.6 | +3.2 | +4.5 |

Source: Credit Sesame surveyed 600 Americans on how their credit scores improved with the addition of new financial products. Participants were divided by credit ranking and further categorized by the type of financial product they purchased (credit cards, merchant credit cards, car loans, and mortgage loans). The study was conducted August 2015 and concluded August 2017.

If you do not currently have a wide mix of credit, adding a new credit card or a store card could give you an added boost. And, as we mentioned before, this will also help improve your credit utilization.

Consider becoming an authorized user

Another strategy for improving your credit using credit cards is to become an authorized user on another person’s account. Most often, this is a parent with good credit who trusts you to be a responsible user on their existing credit card.

When you become an authorized user, their credit history (related to that card) is reflected on your credit report —essentially giving you an added boost in credibility. This can also help improve your credit utilization.

Average Credit Score Improvement as an Authorized User

| Credit Starting Point | 3 Months | 6 Months | 12 Months |

|---|---|---|---|

| Bad (550<) | +16 | +27 | +43 |

| Poor (550+) | +10 | +21 | +32 |

| Fair (600+) | +6 | +15 | +21 |

| Good (650+) | +6 | +11 | +17 |

| Very Good (750+) | +8 | +9 | +12 |

| Excellent (800+) | +4 | +6 | +8 |

Source: Review of 600 individuals who for the course of a year after being made an authorized user. The study was conducted in February of 2016 and concluded April of 2016.

As you can see from the data above, consumers of all credit ranges were able to increase their score over time by using this strategy. The biggest increase was among those with bad credit (550-600). They were able to increase their score by 43 points in 12 months.

Apply for a secured credit card

A secured credit card is another great option for rebuilding or improving your credit. A secured credit card is backed by a cash deposit that you make when you open the account. The deposit is typically equal to your credit line. If you make a $500 deposit, you’ll have a $500 limit.

The deposit reduces the risk to the creditor because if you don’t pay your bill, they can take the money from the deposit. Often, secured credit cards are available to people with bad or no credit at all.

Building Credit with a Secured Credit Card

| Credit Starting Point | 3 Months | 6 Months | 12 Months |

|---|---|---|---|

| Bad (550<) | +7 | +12 | +25 |

| Poor (550+) | +5 | +10 | +19 |

| Fair (600+) | +3 | +8 | +15 |

| Good (650+) | +2 | +7 | +11 |

| Very Good (750+) | +0 | +5 | +9 |

| Excellent (800+) | +0 | +2 | +7 |

Source: Review of 600 individuals who for the course of a year who had a secure credit card. The study was conducted in February of 2016 and concluded April of 2016.

As you can see from the data above, adding a secured credit card was a great strategy for those with poor and fair credit. In the case of individuals with poor credit, they were able to increase their score 25 points in 12 months, whereas those with fair credit were able to increase their score 19 points in the same timeframe

.

Review and monitor your credit report

As we previously discussed, it’s important to check your credit report so you are aware of what it contains, but it’s also important to review and monitor your credit periodically as you’re trying to rebuild or improve it.

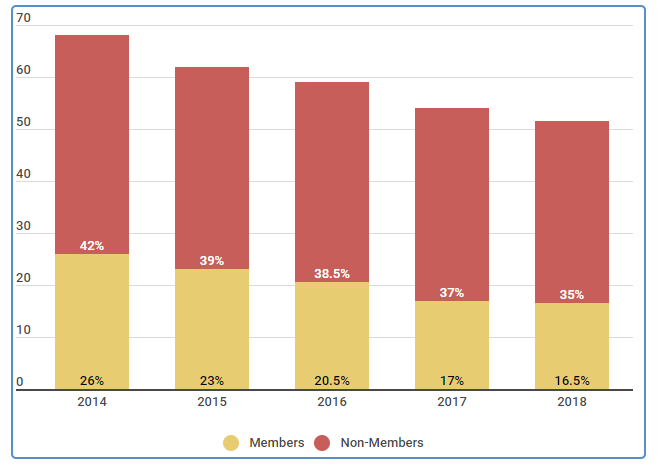

As you can see from the data below, 17% of Credit Sesame members found credit report inaccuracies when they checked their report. Clearing up these inaccuracies by filing disputes with the creditor can have a big impact on your score.

Percentage of Individuals who found Credit Report Inaccuracies

| Found Inaccuracies on Credit Report | Members | Non-Members |

|---|---|---|

| 2014 | 26% | 42% |

| 2015 | 23% | 39% |

| 2016 | 20.5% | 38.5% |

| 2017 | 17% | 37% |

| 2018 | 16.5% | 35% |

Source: Survey of 500 members and non-members who check their credit reports yearly. Survey was done in October annually.

f the credit bureau resolves the issue in your favor, your credit score will likely rise. Here are some common credit report errors and the average increase over time to your credit score. It is always a good idea to resolve any errors you find as soon as you can.

Benefits of learning how to use credit cards the right way

Learning how to use credit cards to rebuild or improve your credit is important because not only can you use those tactics and strategies to improve your credit profile, you can continue using them to make sure your credit stays great in the long run.

In addition to the points we’ve outlined above, also consider the following tips as best-practices when it comes to using credit cards:

- Pay off your balance in full each month —you can avoid carrying a heavy debt load by trying not to charge anything you can’t pay for in cash.

- Avoid the temptation of free offers —when you apply for new lines of credit, your credit is pulled and having additional inquiries can lower your score.

- Keep your accounts open —the age of your credit is another factor that impacts your score so be sure to keep open your longest-standing accounts

If you’re looking to improve your credit score, these strategies, along with patience and time, will help you not only with short-term increases, but also long-term improvement.

Conclusion & Summary

To sum it up, rebuilding your credit using credit cards can be a great strategy for success —considering that many of the factors used to calculate your credit score revolve around using credit cards the right way. You can take steps like making your payments on time, lowering your credit utilization, mixing up your credit types, becoming an authorized user, and others to make these improvements. When you learn how to use credit cards to your benefit, you’ll see results both in the short- and long-term.