If you’ve recently checked your credit and discovered that your credit score is 680, congrats. You’ve taken the first step into taking better care of your credit health by looking into your credit report and knowing your score. But do you really know what a 680 credit score means?

Basics of a 680 credit score

While there are a number of different models for calculating your credit score, we’re going to focus on the FICO Score, since it is the most widely recognized and accepted model. Your FICO Score is a three-digit number that is designed to act as a snapshot of your creditworthiness – a way for potential lenders to quickly understand how likely you are to pay your debts as promised. FICO scores range from 300 to 850, with higher numbers representing better credit scores.

Scores from approximately 680 to 739 mark are considered to be in the Good credit score range. If you have a credit score of 680, you will likely be approved for a loan or a credit card — and you can expect to be offered moderate interest rates. Lenders are more comfortable with borrowers who fall in this credit score range, making the decision to extend credit much easier.

As you can see from the data below, most people under the age of 30 have a credit score below 679, while roughly 33 percent have a 680 or higher.

U.S. Population Categorized by FICO Range & Credit Scores

| Age | < 580 | 580 - 669 | 670 - 739 | 740 - 799 | 800 > |

|---|---|---|---|---|---|

| Under 30 | 29% | 38% | 17% | 11% | 5% |

| 30 - 39 | 35% | 24% | 10% | 16% | 15% |

| 40 - 49 | 26% | 24% | 10% | 17% | 23% |

| 50 - 59 | 19% | 22% | 10% | 17% | 32% |

Source: We ran a survey of 550 US consumers in different age groups on 9/26/2018 to understand which credit score ranges they fell into.

Now that you know the basics of the 680 credit score, let’s take a look at what it means, as well as what you can do to take your credit score to the next level.

How to improve your 680 credit score

Even with Good credit, there are always steps that you can take to help build and improve your credit. To help improve your credit score, you’ll want to focus on the following strategies.

- Reduce your debt

- Lower your credit utilization to below 30 percent

- Limit the number of hard inquiries

- Don’t apply for any new lines of credit

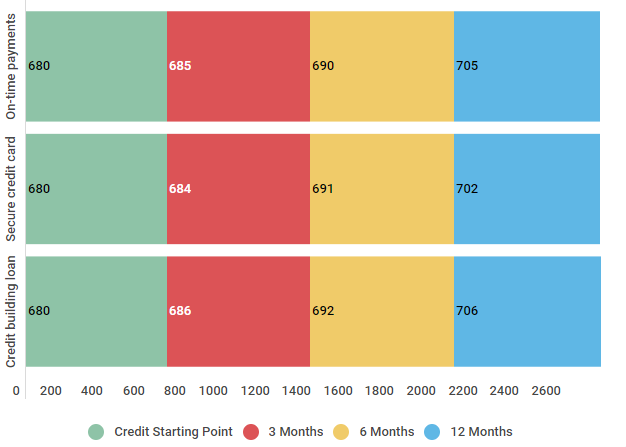

As we’ll discuss in the next section, these strategies directly align with the factors that make up your credit score. The data below shows the average increase you can expect to see over three months, six months and 12-months if you take these steps.

Average Credit Score Improvement starting with Good credit

| Method | Credit Starting Point | 3 Months | 6 Months | 12 Months |

|---|---|---|---|---|

| On-time payments | 680 | 685 | 690 | 705 |

| Secure credit card | 680 | 684 | 691 | 702 |

| Credit building loan | 680 | 686 | 692 | 706 |

Source: Review of 600 individuals increased their credit by different methods The study was conducted in February of 2016 and concluded in April of 2016.

Let’s look at how these credit-improvement strategies align with the factors that determine your credit score.

Factors that determine your credit score

In order to fully understand your credit score, let’s take a closer look at what goes into building it:

- Payment History. As you can see below, your payment history is the single biggest piece of your credit score puzzle. Always make your payments on time — every time. This will go a long way toward having the best score possible.

- Credit Utilization. The next biggest piece is your credit utilization or, in other words, the percentage of your available credit that you’re currently using. To improve your score, keep this number as low as possible. Experts recommend 30 percent or less, but the best credit scores are often a reflection of 10 percent or less.

- Credit Age. The age of your credit history is also important to potential lenders. They want to see a long-standing history of responsible use with credit, so be sure to keep your oldest accounts open.

- Different Types of Credit. Lenders also like to see a mix of different types of credit on your credit report. In other words, it’s better to not only have consumer credit cards, but also an auto loan, mortgage loan, student loan, or something similar.

- Number of Inquiries. This is the smallest piece of the puzzle, but it can definitely hurt your score if you have too many inquiries. While a soft inquiry, such as when you check your own credit, won’t hurt your score — a hard inquiry, such as when applying for a new line of credit, will. Try to limit this number, if possible.

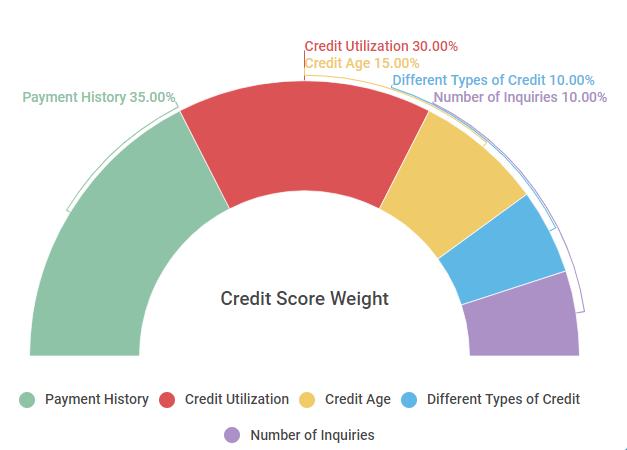

Below, you can see how each of these factors is weighted when calculating your credit score. Payment history and credit utilization certainly have the biggest impact, while things like the number of inquiries on your report and your credit mix each are weighted around 10 percent.

FICO Scoring Model Calculation (Weight) Factors

| Credit Factors | Credit Score Weight |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Different Types of Credit | 10% |

| Number of Inquiries | 10% |

Source: https://www.myfico.com/credit-education/whats-in-your-credit-score

By knowing what impacts your 680 credit score, you can make a conscious effort to improve it. But, what if you don’t have the time and you want to know what your 680 score can get you right now? Keep reading

What can you expect with a 680 credit score?

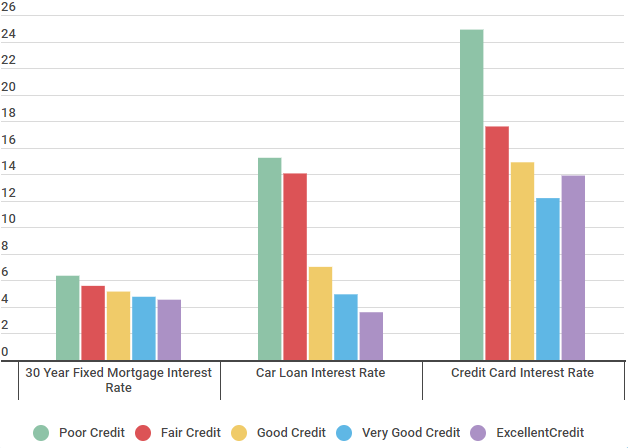

Your 680 credit score is right on the verge of being considered Good credit, as opposed to Fair credit. Take a look at the average interest rates below — while it may not seem like a lot to save a couple percentage points here or there on interest rates, the data shows otherwise.

Consider the data below. Someone with Fair credit is likely to get a 14.06 percent interest rate on a car loan, whereas someone with Good credit may see a rate around 7.02 percent.

If you finance a $15,000 car over 60 months with Fair credit and a rate of 14.06 percent, that car will cost you $20,969 by the time you’ve paid it off. On the other hand, at a 7.02 percent interest rate, that same car will cost you $17,830. Now, if you were able to improve your credit score to Very Good (4.95 percent), that car would cost $16,964. That is a savings of right around $4,000 between Fair and Very Good.

Average Interest Rate Ranges Rates Divided by Credit Score Range

| Type of Loan | Poor Credit | Fair Credit | Good Credit | Very Good Credit | Excellent Credit |

|---|---|---|---|---|---|

| 30 Year Fixed Mortgage Interest Rate | 6.352% | 5.588% | 5.158% | 4.767% | 4.545% |

| Car Loan Interest Rate | 15.24% | 14.06% | 7.02% | 4.95% | 3.60% |

| Credit Card Interest Rate | 24.9% | 17.6% | 14.9% | 12.2% | 13.9% |

Source: Credit Sesame asked 400 members about their interest rates during a three week period beginning on January 18, 2018.

When you look at the data, it’s clear to see how even just a small change in your credit score can make a big impact on your wallet. Now, let’s look at one of the most important steps you can take the improve your score — dealing with negative information.

| Free credit score |

|---|

| 680 credit score |

| How to improve your credit score |

| What is a good credit score |

| Perfect credit score |

| Fico score |

Dealing with negative information on your credit report

Utilizing the tips owe spoke about earlier outlined above will help to improve your credit score, but first, you’ll want to check your credit report to see what information it contains. Keep in mind these reports aren’t perfect — more than an estimated 30 percent of credit reports contain errors or inaccuracies.

Of course, some of the negative information in your account may be accurate. Either way, do you know what kind of negative information could be found in your credit report and the impact they can have on your score?

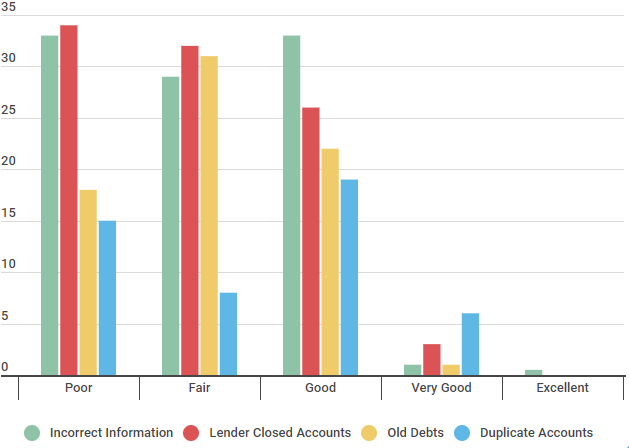

The chart below shows some of the most common errors and the percentage of Credit Sesame members (at various stages of credit rankings) that saw these errors on their reports.

Errors which affect credit rankings

| Credit Ranking | Incorrect Information | Lender Closed Accounts | Old Debts | Duplicate Accounts |

|---|---|---|---|---|

| Poor | 33% | 34% | 18% | 15% |

| Fair | 29% | 32% | 31% | 8% |

| Good | 33% | 26% | 22% | 19% |

| Very Good | 1% | 3% | 1% | 6% |

| Excellent | 0.5% | N/A | N/A | N/A |

Source: Credit Sesame surveyed 250 people, 50 had a poor credit ranking, 50 participants had a Fair credit score, 50 members had a Good credit rating, 50 people were listed as Very Good, and 50 members reported they had an Excellent credit score. The study was conducted on October 20, 2017, over a period of two weeks.

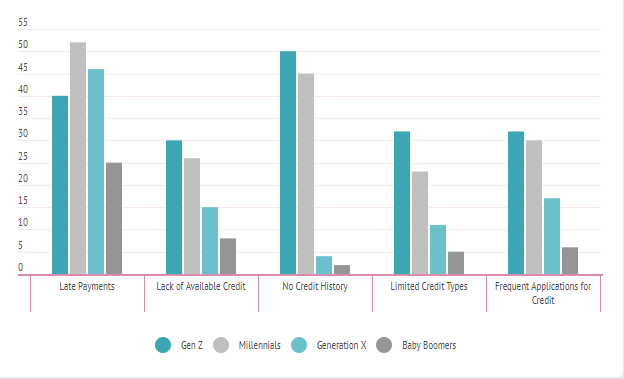

And, before you’re too hard on yourself, keep this in mind — these negative factors don’t discriminate. Take a look below at how the different generations stack up when it comes to having negative information in their reports:

Negative Factors that Contribute to Low Credit Scores

| Negative Factors | Millennials | Generation X | Baby Boomers |

|---|---|---|---|

| Late Payments | 52% | 46% | 25% |

| Lack of Available Credit | 26% | 15% | 8% |

| No Credit History | 45% | 4% | 2% |

| Limited Credit Types | 23% | 11% | 5% |

| Frequent Applications for Credit | 30% | 17% | 6% |

Source: Credit Sesame polled 400 participants between February 10, 2018, and February 17, 2018. 100 participants were Gen Z, 100 participants were Millennials, 100 participants were Gen X, and 100 participants were Baby Boomers.

The first step to improving your credit is to make sure that all the information on your current credit report is accurate. File a dispute if there are any inaccuracies; accurate information can’t be removed until it cycles off. Improve your previous negative habits and replace them with better ones:

- Bring any overdue accounts current

- Pay any liens (if necessary)

- Work with collection agencies and creditors to clear up any collections

- Don’t apply for any new lines of credit

- Pay down current debt as soon as possible

- Pay all of your bills on time, every time

How Irving improved his 680 credit score to 722 in 18 months

Member Since: 4/26/2016

We interviewed Irving on May 18, 2018; he earns $51,000 a year, is 30 years old and lives in Houston, Tex. He is single and currently rents an apartment.

TLDR; what can you do with a 680 credit score?

Patience and time, along with the proper steps and action, can improve even Fair or Good credit scores. By practicing good credit habits consistently, the impact of any negative information contained in your credit report will lessen. As these negative items cycle off your credit report, you will see your score continue to rise — and enjoy the many benefits that come with better credit.