According to the Boston Fed, nearly 80 percent of U.S. adults have a credit card. For many, using credit cards can be an excellent way to build credit and a convenient way to pay for necessary expenses without using cash or checks. For others, credit cards encourage a pattern of overspending, leading to high fees, debt, and a damaged credit score.

It’s estimated that more than half of cardholders in the U.S. revolve their debt. Unlike credit card “transactors,” who use their cards for purchases and pay off the balance each month, credit card “revolvers” carry balances on their cards and accumulate interest along the way. When a cardholder cannot make the minimum payment on their card, it is known as delinquency. The flow into 90+ day delinquency for credit card balances has been increasing notably for the last year, indicating that fewer cardholders can pay off the amount they owe.

One of the biggest risk factors for delinquency is credit utilization—how close someone is to maxing out their credit card. To better understand the state of credit card debt across the country, researchers from Credit Sesame analyzed its own data and data from the Federal Reserve Bank of New York. Rather than looking at overall or per-capita credit card debt (as many other studies do), its researchers decided to look at credit utilization, or debt as a proportion of available credit, which also happens to be one of the most important factors affecting a person’s credit score. According to Credit Sesame, people with the best credit scores—over 800—use no more than 7% of their available credit.

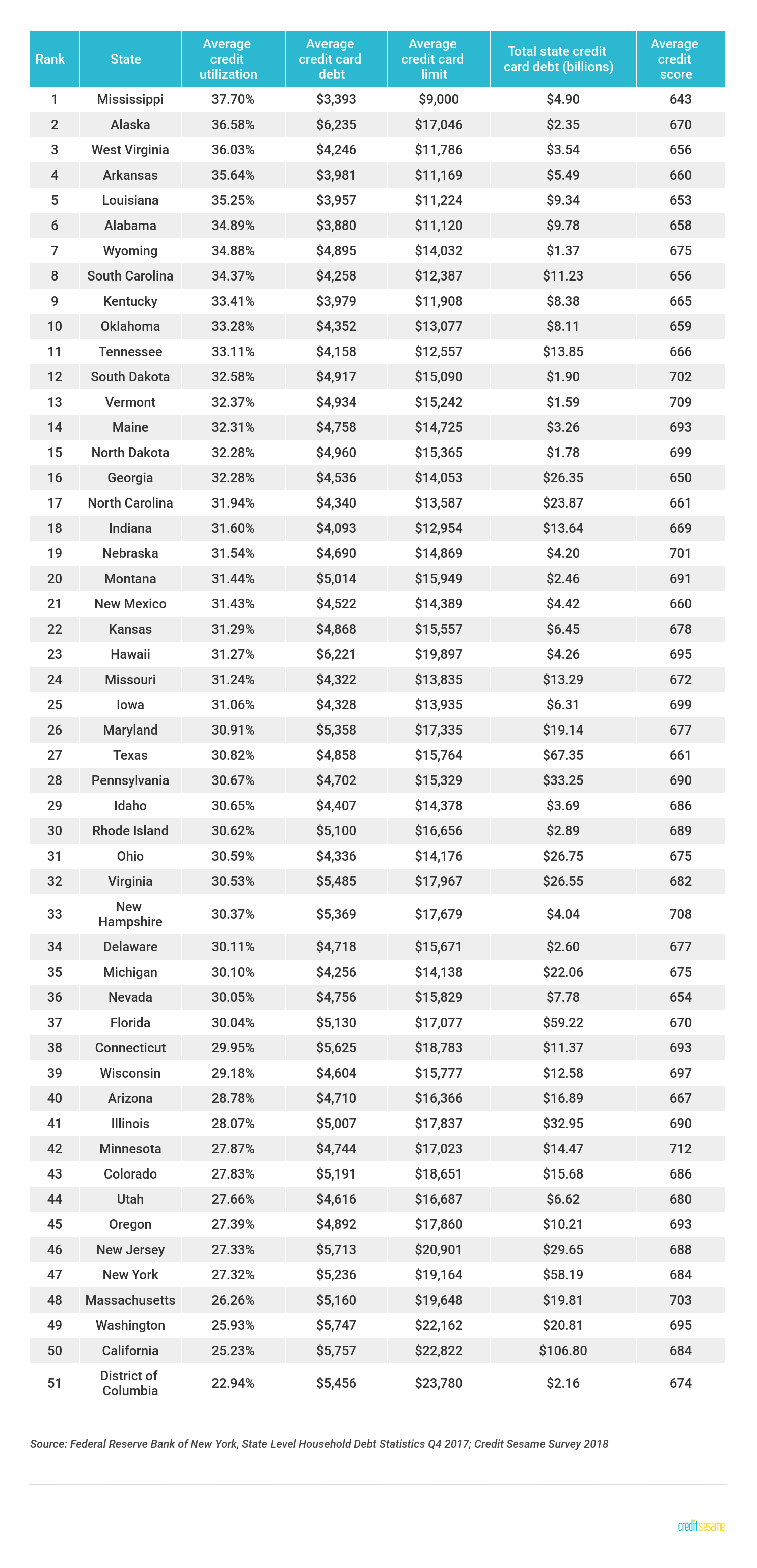

The research indicates that the national average credit card limit is $16,737 and the average credit card debt is $4,903, which yields an average credit utilization ratio of 29%. However, these figures vary significantly from state to state. The difference in average credit utilization between the top 10 states with the highest and lowest credit utilization is 8.5 percentage points. Correspondingly, the difference in average credit score between the top 10 states with the highest and lowest credit card utilization is 31 points. The states that max out their credit cards the most tend to be located in the south, have a larger rural population, and have lower credit card limits. Here are the states using the most and least of their available credit.

States Using the Most of Their Available Credit

10. Oklahoma

- Average credit utilization: 33.28%

- Average credit card debt: $4,352

- Average credit card limit: $13,077

- Total state credit card debt: $8.11 billion

- Average credit score: 659

9. Kentucky

- Average credit utilization: 33.41%

- Average credit card debt: $3,979

- Average credit card limit: $11,908

- Total state credit card debt: $8.38 billion

- Average credit score: 665

8. South Carolina

- Average credit utilization: 34.37%

- Average credit card debt: $4,258

- Average credit card limit: $12,387

- Total state credit card debt: $11.23 billion

- Average credit score: 656

7. Wyoming

- Average credit utilization: 34.88%

- Average credit card debt: $4,895

- Average credit card limit: $14,032

- Total state credit card debt: $1.37 billion

- Average credit score: 675

6. Alabama

- Average credit utilization: 34.89%

- Average credit card debt: $3,880

- Average credit card limit: $11,120

- Total state credit card debt: $9.78 billion

- Average credit score: 658

5. Louisiana

- Average credit utilization: 35.25%

- Average credit card debt: $3,957

- Average credit card limit: $11,224

- Total state credit card debt: $9.34 billion

- Average credit score: 653

4. Arkansas

- Average credit utilization: 35.64%

- Average credit card debt: $3,981

- Average credit card limit: $11,169

- Total state credit card debt: $5.49 billion

- Average credit score: 660

3. West Virginia

- Average credit utilization: 36.03%

- Average credit card debt: $4,246

- Average credit card limit: $11,786

- Total state credit card debt: $3.54 billion

- Average credit score: 656

2. Alaska

- Average credit utilization: 36.58%

- Average credit card debt: $6,235

- Average credit card limit: $17,046

- Total state credit card debt: $2.35 billion

- Average credit score: 670

1. Mississippi

- Average credit utilization: 37.70%

- Average credit card debt: $3,393

- Average credit card limit: $9,000

- Total state credit card debt: $4.90 billion

- Average credit score: 643

States Using the Least of Their Available Credit

10. Minnesota

- Average credit utilization: 27.87%

- Average credit card debt: $4,744

- Average credit card limit: $17,023

- Total state credit card debt: $14.47 billion

- Average credit score: 712

9. Colorado

- Average credit utilization: 27.83%

- Average credit card debt: $5,191

- Average credit card limit: $18,651

- Total state credit card debt: $15.68 billion

- Average credit score: 686

8. Utah

- Average credit utilization: 27.66%

- Average credit card debt: $4,616

- Average credit card limit: $16,687

- Total state credit card debt: $6.62 billion

- Average credit score: 680

7. Oregon

- Average credit utilization: 27.39%

- Average credit card debt: $4,892

- Average credit card limit: $17,860

- Total state credit card debt: $10.21 billion

- Average credit score: 693

6. New Jersey

- Average credit utilization: 27.33%

- Average credit card debt: $5,713

- Average credit card limit: $20,901

- Total state credit card debt: $29.65 billion

- Average credit score: 688

5. New York

- Average credit utilization: 27.32%

- Average credit card debt: $5,236

- Average credit card limit: $19,164

- Total state credit card debt: $58.19 billion

- Average credit score: 684

4. Massachusetts

- Average credit utilization: 26.26%

- Average credit card debt: $5,160

- Average credit card limit: $19,648

- Total state credit card debt: $19.81 billion

- Average credit score: 703

3. Washington

- Average credit utilization: 25.93%

- Average credit card debt: $5,747

- Average credit card limit: $22,162

- Total state credit card debt: $20.81 billion

- Average credit score: 695

2. California

- Average credit utilization: 25.23%

- Average credit card debt: $5,757

- Average credit card limit: $22,822

- Total state credit card debt: $106.80 billion

- Average credit score: 684

1. District of Columbia

- Average credit utilization: 22.94%

- Average credit card debt: $5,456

- Average credit card limit: $23,780

- Total state credit card debt: $2.16 billion

- Average credit score: 674

Methodology & Full Results

The data used in this analysis is from a sample of over 3.5 million Credit Sesame users across the United States, updated in June 2018. User-level data on credit card debt, limits, and utilization was used to compute state-level averages. States were ranked by their average credit utilization. The median credit score for each state was sourced from the Credit Sesame’s Credit Score Survey from January 2018. The scores shown are VantageScores. Total state credit card debt was sourced from the Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit Q4 2017.